Peptide Merchant Account: Why Banks Keep Dropping You and How Crypto Infrastructure Fixes It

If you run a peptide business, you already know the drill. You spend weeks getting approved by a high-risk processor. You integrate their API, update your checkout, start processing volume — and then three months later you get an email saying your account is being terminated "due to business risk." No appeal. No timeline. Just a merchant ID that stops working by end of week.

This isn't bad luck. It's structural. The traditional banking stack — acquiring banks, card networks, payment processors — is optimized for low-risk, easily categorized businesses. Peptide merchants, research chemical sellers, and adjacent supplement companies sit in a legal gray zone that acquiring banks want nothing to do with, regardless of whether your business is operating legally and responsibly. The risk isn't about you personally. It's about their exposure.

Teams think the problem is finding a more lenient processor. The real problem is that any architecture built on a single acquiring relationship is one compliance review away from going dark. That's the actual architecture failure.

This guide is about reframing the peptide merchant account problem as an infrastructure decision — specifically, how crypto payment infrastructure gives you a processing layer that doesn't terminate on you, and what it actually takes to build that in production.

Table of contents

- Why peptide merchant accounts keep getting terminated

- The architecture problem nobody talks about

- Why crypto is the right architecture layer for peptide merchants

- Choosing the right crypto payment gateway

- Integration architecture for peptide merchants

- Handling fiat conversion and treasury risk

- Compliance considerations that still apply

- Common failure modes when peptide merchants integrate crypto

- Escrow and trust signals for customers

- Running crypto alongside fiat — the dual-stack approach

- Where CoinPayPortal fits in this architecture

Why peptide merchant accounts keep getting terminated

The termination cycle for peptide merchants is predictable enough that most experienced operators treat it as a recurring cost of doing business. Getting approved, integrating, and then getting dropped is so common that it has become a background assumption in the industry. Understanding why it happens is the first step to architecting around it.

The acquiring bank's incentive structure

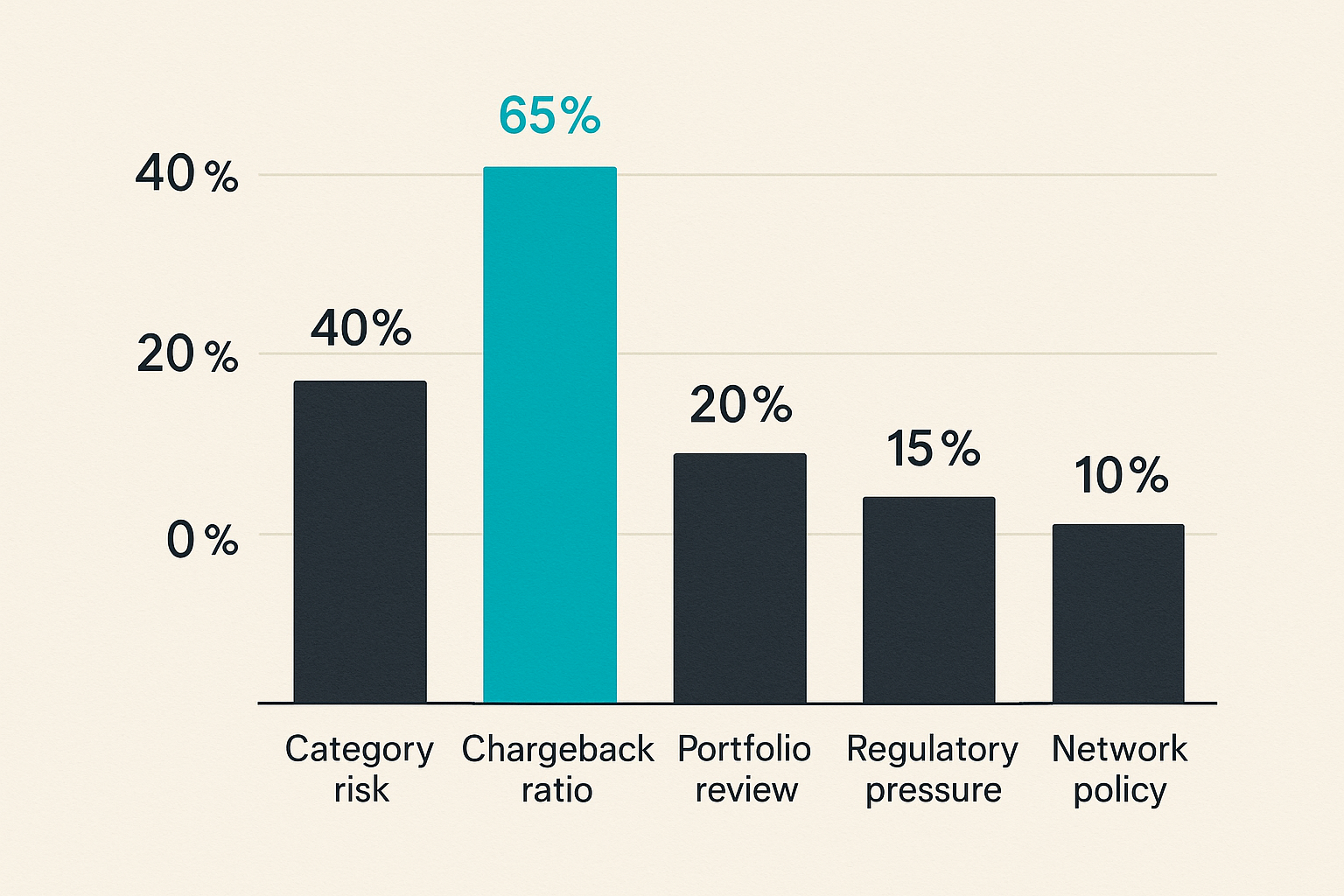

Acquiring banks are responsible for the merchants they onboard. When a merchant gets a chargeback, files a dispute, or draws regulatory attention, the acquiring bank is in the chain of liability. Card networks like Visa and Mastercard monitor acquirer chargeback ratios at the portfolio level — if an acquirer's ratio across their merchant portfolio crosses certain thresholds, the card network can fine or sanction the acquirer directly.

This means the acquirer's incentive is to minimize exposure, not to evaluate your business on its merits. Peptides exist in a space where the regulatory landscape is genuinely ambiguous — some peptides are research chemicals, some are prohormones, some are borderline supplements, and the FDA's position shifts. Acquirers don't want to hold that ambiguity. They'd rather drop the category entirely.

How category codes and underwriting work against you

Every merchant account gets assigned a Merchant Category Code (MCC). Peptide and research chemical businesses often get assigned to categories that are already flagged as high-risk — nutraceuticals, dietary supplements, or in some cases pharmaceutical-adjacent codes. These codes trigger tighter underwriting, rolling reserves (often 5–10% held for 180 days), and more frequent account reviews.

The practical consequence: even if you're approved and processing fine, a routine portfolio review by the acquirer's risk team can result in termination with no chargeback history to justify it. Underwriters flag the category, not the merchant. That's the structural trap.

Practical rule: Any merchant account in a high-risk MCC category should be treated as temporary infrastructure. Build your fulfillment and operations to survive 30-day disruptions. If your business can't survive a processor termination for a month, the architecture is fragile.

The architecture problem nobody talks about

Most of the advice for peptide merchants focuses on finding better processors — offshore acquirers, high-risk specialists, or stacked merchant accounts. That advice isn't wrong, but it addresses the symptom rather than the root. The problem is dependency.

Single-processor dependency is a single point of failure

A checkout that can only process cards through one acquiring relationship is a single point of failure by definition. When that relationship ends — and for peptide merchants, it will end — your revenue stops. Every hour of downtime while you scramble to integrate a new processor is revenue lost and customer trust damaged.

The mistake teams make is treating payment processing as a commodity utility and building accordingly. You wire up one API, put it in production, and move on to building other things. That model works for Shopify stores selling phone cases. It does not work for businesses in legally contested categories.

What resilient payment infrastructure actually looks like

Resilient payment infrastructure for high-risk categories has at least two independent processing layers — ideally with different underlying mechanisms, not just different processors using the same card rails. If both your "primary" and "backup" processors use Visa/Mastercard acquiring, a card network policy change can take out both simultaneously.

Crypto is the natural second layer precisely because it operates on different rails entirely. A blockchain-based payment gateway doesn't have an acquiring bank. There's no underwriting review, no MCC classification, no chargeback system to trigger portfolio-level sanctions. The acceptance criteria are defined by the protocol, not by a risk committee.

Practical rule: Your crypto payment layer isn't a backup for when cards fail. It's the layer that remains when your acquiring relationship ends. Design for that, not for the nice-to-have case.

Why crypto is the right architecture layer for peptide merchants

The argument for crypto in high-risk merchant contexts is often framed around ideology — decentralization, censorship resistance, financial freedom. That framing is counterproductive for operators. The real argument is structural and practical.

Censorship resistance is not a political argument

When people in fintech talk about censorship resistance, they mean something specific: a payment network where no single intermediary can unilaterally decide to stop processing your transactions. Bitcoin, Ethereum, and most production-viable blockchains have this property at the protocol level. No acquiring bank can terminate your address. No card network can blacklist your category.

For a peptide merchant, this is not an ideological preference. It's the difference between a payment infrastructure that can be switched off by a third party's policy decision and one that can't. That's a practical engineering property, the same way "no single point of failure" is a practical engineering property.

Non-custodial vs custodial: why custody boundaries matter

Not all crypto payment solutions have the same architecture. A custodial crypto processor holds your funds between payment receipt and settlement — meaning they can, in practice, freeze or delay payouts if they decide to. Some custodial crypto processors have done exactly this for high-risk merchants. The censorship resistance you thought you were buying disappears the moment a custodian decides to enforce their own policies.

Non-custodial infrastructure means funds go directly to wallets you control. The gateway facilitates the payment detection and confirmation logic; it doesn't intermediate the money. For peptide merchants specifically, non-custodial is the only architecture that actually delivers on the stability promise. As we covered in our detailed guide to peptide payment infrastructure, the custody boundary is where most teams make the wrong call.

Choosing the right crypto payment gateway

Not every gateway marketed as "crypto payments" is built for merchant production use. Many are consumer-focused wallets with a checkout widget bolted on. Others are custodial services that happen to accept crypto. The practical question is: what does this gateway actually do in production, and where are the failure surfaces?

What to look for beyond "we accept crypto"

When evaluating a crypto payment gateway for a peptide merchant account alternative, the relevant criteria are:

- Non-custodial by default: funds flow to your wallet, not through a third-party float.

- Address derivation: the gateway should generate unique deposit addresses per order, not reuse addresses across transactions. Address reuse causes reconciliation nightmares at volume.

- Webhook reliability: you need reliable order status callbacks with retry logic. Payment confirmation on-chain doesn't guarantee a webhook delivery.

- Confirmation depth configuration: different risk tolerances require different confirmation counts. A gateway that hardcodes one confirmation for all transactions is not production-grade.

- Stablecoin support: merchants who can't hold crypto volatility exposure need USDC or USDT settlement paths.

- Multi-chain support: customers use different chains. Ethereum, Solana, and Lightning Network coverage matters for conversion rates.

The CoinPay documentation covers these integration specifics in detail for developers building against the API.

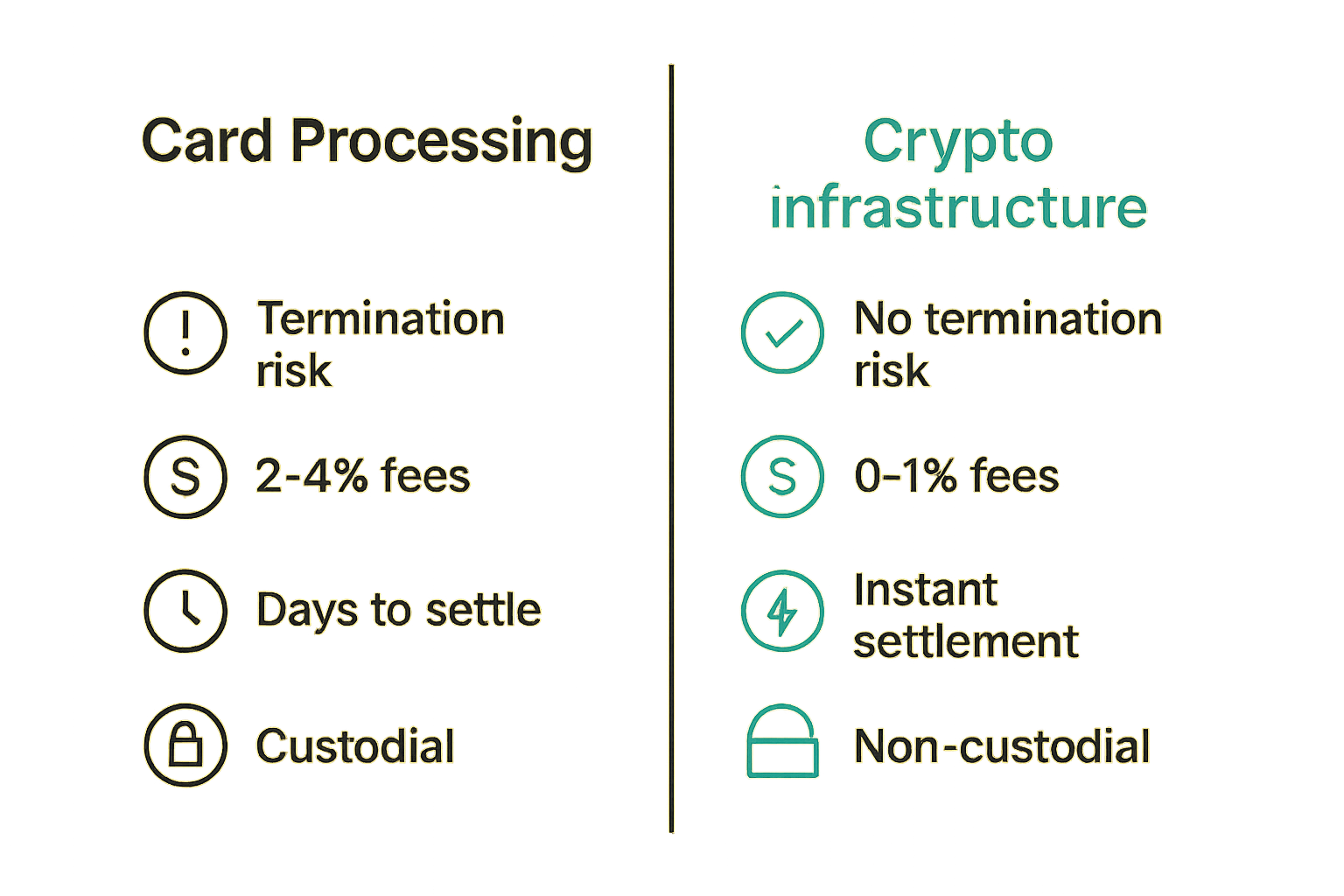

Comparison: custodial vs non-custodial gateways

| Feature | Custodial Gateway | Non-Custodial Gateway |

|---|---|---|

| Funds control | Gateway holds funds | Merchant wallet receives directly |

| Termination risk | Gateway can freeze payouts | No custodial relationship to terminate |

| KYC/AML burden | Gateway-level KYC on merchant | Merchant-level responsibility |

| Setup complexity | Lower (managed) | Moderate (wallet management required) |

| Settlement speed | Depends on gateway payout schedule | Confirmation depth only |

| Chargeback exposure | Sometimes (gateway-dependent) | None — crypto transactions are final |

| High-risk category suitability | Risky — policy-dependent | Strong — no category review |

Practical rule: Evaluate a custodial crypto gateway with the same skepticism you'd apply to any acquiring relationship. If the gateway can freeze your funds for policy reasons, you've replicated the same risk in a different wrapper.

Integration architecture for peptide merchants

Getting crypto payment processing right in production requires more than pointing a checkout to a crypto address. The integration has three distinct layers that each need to be thought through: checkout flow, webhook state management, and reconciliation.

Checkout flow and wallet address generation

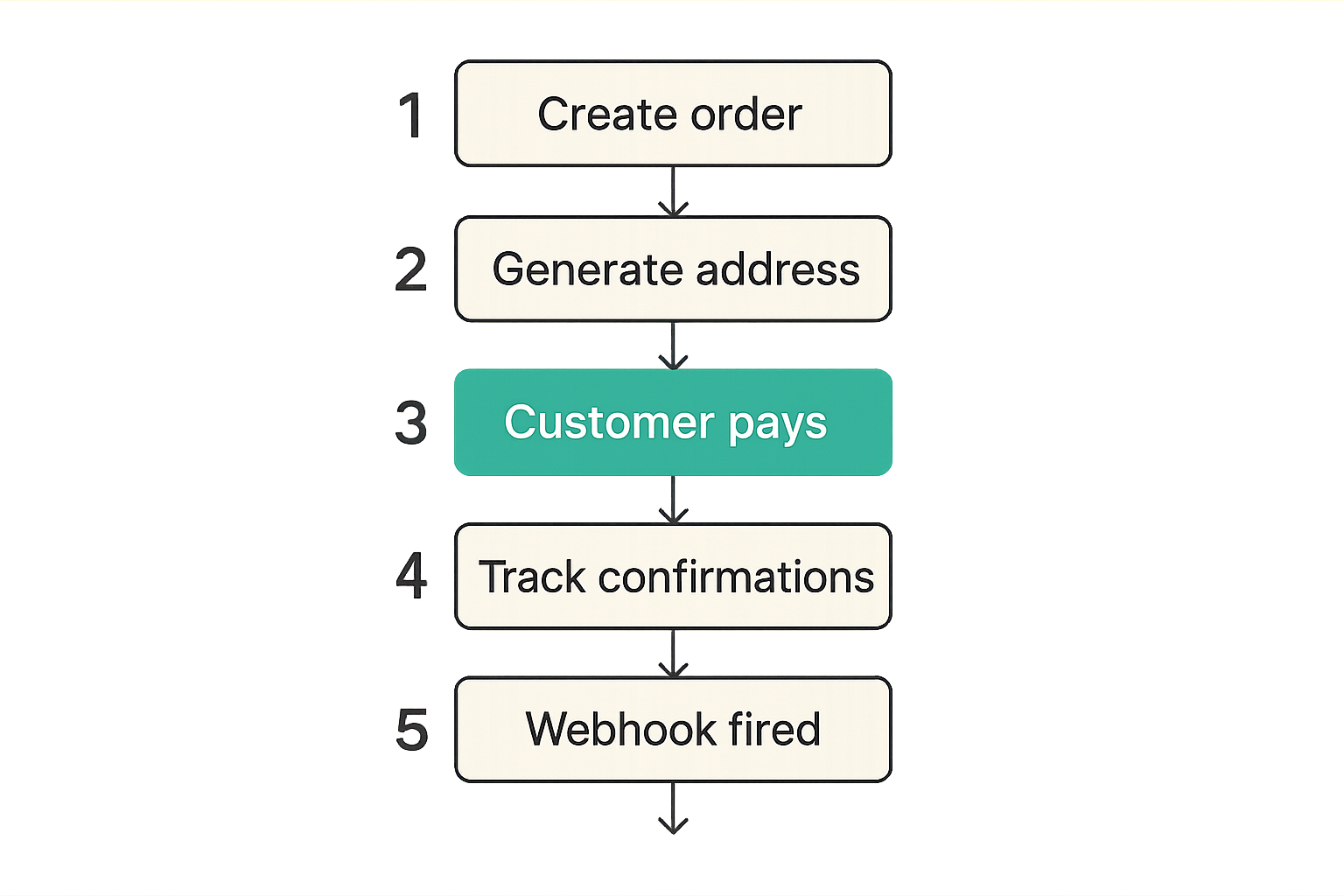

The basic flow looks like this:

- Customer initiates checkout and selects crypto payment.

- Your backend calls the payment gateway API to create a payment intent, specifying currency, amount in fiat or crypto, and order metadata.

- The gateway returns a unique deposit address and payment amount (with conversion rate lock, if applicable).

- Your checkout displays the address and QR code with a payment window timer.

- Customer broadcasts transaction from their wallet.

- Gateway detects the on-chain transaction and begins confirmation tracking.

- Gateway fires webhook events:

payment_detected,payment_confirmed,payment_complete. - Your backend updates order state based on webhook events.

- Order enters fulfillment pipeline.

The payment window is a practical concern. Crypto transactions can sit in mempool during congestion. A 15-minute window is too short for Bitcoin during high-fee periods. A 60-minute window is standard; for high-value orders, some merchants extend to 90 minutes with a displayed countdown.

Webhook state management and confirmation depth

What breaks in practice here is treating the payment_detected event as equivalent to payment_confirmed. Detection means the transaction is in the mempool — it can still be replaced or dropped. Confirmation means the transaction is in a block. The appropriate confirmation depth depends on order value and chain.

For Ethereum, 12 confirmations is the common production standard. For Bitcoin, 3–6 depending on order value. For Lightning Network, payment is final upon receipt — no confirmation depth applies. For stablecoins on lower-fee chains (Polygon, Solana), 1–3 confirmations is typically sufficient given the economics of attacking those chains.

Your order state machine should model these stages explicitly: payment_pending, payment_detected, payment_confirming, payment_complete, payment_expired, payment_failed. Conflating any two of these stages will cause fulfillment errors at scale. The crypto payment gateway architecture guide covers this state machine in detail for teams building their own integration layer.

Reconciliation and order fulfillment logic

Crypto payments are immutable once confirmed, but your order records aren't. Reconciliation means ensuring every on-chain confirmed payment maps to exactly one fulfilled order, and every fulfilled order has an on-chain confirmed payment backing it.

The common failure mode: a customer pays twice (sends the same amount to the same address because they thought the first tx failed), and your system creates two orders or credits one order twice. Address-per-order architecture prevents this — each order gets a unique deposit address, so double payments are detectable as overpayment rather than ambiguous.

Build a reconciliation job that runs independently of your webhook handler. The webhook is the fast path; the reconciliation job is the correctness check. Scan confirmed transactions for your addresses against open orders, flag discrepancies, and alert your ops team.

Handling fiat conversion and treasury risk

Most peptide merchants have fiat cost structures — suppliers, staff, logistics. Holding received crypto as-is means carrying volatility risk. Figuring out how to get value from crypto receipts into your operating accounts is a real operational problem, not a theoretical one.

On-ramp and off-ramp options in 2026

The off-ramp landscape has matured significantly. The practical options for peptide merchants in 2026 are:

- Crypto-to-fiat OTC desks: better rates than exchanges for volume above $10k/month, but require KYB (know your business) onboarding.

- Regulated crypto exchanges with business accounts: Kraken, Coinbase Prime, and Bitstamp all offer business accounts with ACH/wire withdrawal. Onboarding takes 1–3 weeks and requires business verification.

- Stablecoin parking: convert incoming crypto to USDC or USDT on-chain, hold in stablecoin until you're ready to off-ramp. Removes volatility exposure without immediately triggering a fiat conversion event.

- Payment processors with built-in conversion: some gateways offer automatic conversion to stablecoin or fiat at point of receipt. Convenient but typically at a 0.5–1.5% spread cost.

The mistake teams make is assuming the off-ramp problem is the gateway's problem. Most non-custodial gateways don't touch your funds, so the conversion is your responsibility. Plan this before going live.

Stablecoins as a settlement layer

The practical architecture for most peptide merchants who can't absorb volatility: accept multiple cryptocurrencies at checkout, immediately swap to USDC via an on-chain DEX or via gateway auto-conversion, hold USDC in a business wallet, off-ramp USDC to fiat weekly or bi-weekly via your exchange business account.

This approach gives you: censorship-resistant payment acceptance, zero crypto volatility exposure, and a manageable treasury workflow. The cost is the conversion spread on incoming payments and the off-ramp fee to fiat. For most merchants, that total cost is 1–2%, which is competitive with high-risk card processing fees (which typically run 3.5–5% plus reserves).

Compliance considerations that still apply

Crypto doesn't make you exempt from compliance obligations. This is worth stating clearly because some merchants adopt crypto with the mistaken belief that blockchain payments are inherently private and unregulated. In 2026, that's not the reality.

AML and KYC obligations for crypto merchants

Depending on your jurisdiction and transaction volume, you may have AML (Anti-Money Laundering) obligations as a crypto merchant, particularly if you're accepting large transactions or operating across multiple jurisdictions. In the US, FinCEN guidance on crypto-accepting merchants has evolved. In the EU, MiCA (Markets in Crypto-Assets) regulation brings crypto commerce into a more defined compliance framework.

The practical guidance: consult with a crypto-aware compliance attorney before scaling. The compliance overhead at low volumes is manageable; at high volumes, ignoring it is a liability. Teams in adjacent high-risk spaces face similar architectural tradeoffs — for example, the DevSecOps community has written about how compliance and security tooling need to be integrated from the start, not bolted on after product-market fit.

Product legality is still your responsibility

Crypto infrastructure cannot make an illegal product legal to sell. If your peptide products are legal for research use in your jurisdiction and you're operating accordingly, crypto payments are a legitimate infrastructure choice. If your products are in a genuinely illegal category, no payment architecture fixes that.

This seems obvious but it's worth stating because some merchants treat payment infrastructure as a compliance bypass. It isn't. What crypto gives you is freedom from a specific form of arbitrary termination — the acquiring bank policy decision. It doesn't change the underlying legal status of your products.

Common failure modes when peptide merchants integrate crypto

What breaks in practice

1. Treating crypto as a bolt-on without updating ops workflows. Crypto payments require different support workflows. A customer who underpays (sends slightly less than required due to exchange rate rounding) needs a manual resolution path. If your support team doesn't have documented procedures for overpayment, underpayment, and stuck transactions, you'll generate customer service failures at volume.

2. Using a custodial crypto processor to replace a custodial card processor. This is the most common failure mode. You've replaced one terminable relationship with another. The termination risk is different but not zero.

3. Hardcoding conversion rates. Crypto prices move. If your checkout calculates the crypto equivalent of a fiat price and holds that for more than a few minutes without a fresh price feed, customers will either overpay or underpay as prices move. Most gateways handle this with a rate lock window; make sure yours does.

4. Not handling mempool congestion. During network congestion, transactions can stay in mempool for hours. A 15-minute payment window will result in payment expiry for transactions that eventually confirm. Your gateway needs to handle "arrived late" transactions gracefully — either extending the window automatically or providing a manual claims path.

5. Ignoring wallet security. Non-custodial means you're responsible for wallet security. Hot wallet key management, cold storage for accumulation wallets, and access controls are now your operational responsibility. Many merchants underestimate this.

What works in production

- Address-per-order architecture with server-side address derivation.

- Explicit order state machines with clear stage transitions.

- Separate webhook fast-path and reconciliation batch job.

- Stablecoin parking to manage volatility exposure.

- Customer-facing payment status page with live confirmation count.

- Support runbooks for edge cases: underpayment, overpayment, expired payment, unconfirmed after 24 hours.

- Multi-chain support to capture customers using different wallets and networks.

Escrow and trust signals for customers

Why trust infrastructure matters for high-risk categories

One underappreciated challenge for peptide merchants adding crypto: customers who are used to card payments also benefit from card protections — chargebacks, fraud disputes, consumer protection regulations. Crypto transactions are final. For a customer who's never ordered from you before, that finality can be a conversion barrier.

The answer isn't to add chargebacks to crypto (that defeats the architecture). The answer is to provide alternative trust signals: verified merchant reputation, escrow options for large orders, and a track record that customers can reference.

Crypto escrow infrastructure — where payment is held in a smart contract pending delivery confirmation — is one solution for high-value orders. The CoinPay escrow product provides this for merchants who need to offer delivery-contingent payment release without reverting to card-based chargeback mechanisms.

Merchant reputation systems also matter. A publicly verifiable payment history and dispute resolution record gives new customers something to evaluate. The CoinPay reputation infrastructure is designed specifically for this — giving merchants in ambiguous categories a trust layer that doesn't depend on a bank's approval.

Running crypto alongside fiat — the dual-stack approach

How to structure fallback and primary processing

The practical recommendation for most peptide merchants isn't to drop cards entirely — it's to build a dual-stack architecture where crypto is a first-class payment option rather than a fallback. Here's why: some customers won't use crypto. Excluding them costs you revenue. But making crypto your primary and most reliable payment layer changes your operational risk profile significantly.

A useful way to think about it: your card processor is your customer convenience layer; your crypto infrastructure is your operational continuity layer. When cards work, they work. When they don't, crypto keeps you running.

Structure the dual-stack like this:

- Checkout: present both options at equal prominence, not crypto as an afterthought. "Pay with card" and "Pay with crypto" as peer options.

- Backend: both payment flows write to the same order management system using the same state machine. Order status, fulfillment, and reconciliation work identically regardless of payment method.

- Reporting: maintain unified revenue reporting across both stacks. Don't run card revenue in one system and crypto revenue in a spreadsheet.

- Reserves: the rolling reserve held by your card processor is a cash flow problem during the integration period. Crypto revenue helps offset that — it arrives without reserve hold.

- Continuity plan: document the procedure for switching checkout to crypto-only mode if your card processor terminates. Practice it before you need it.

Some freelancers and independent operators building out these dual-stack systems have found that job listing intelligence — looking at what payment roles companies are hiring for — gives useful signals about which stacks are becoming table stakes. This writeup on using job listings as market intelligence has some useful tactical framing for that kind of industry research.

As your business grows and your content presence expands, it's also worth thinking about how AI agents and answer engines index your merchant-facing content. This analysis of agentic crawlers and answer engine optimization covers what site owners need to do to stay visible in 2026 — particularly relevant if your product content lives on your merchant site.

Where CoinPayPortal fits in this architecture

Non-custodial infrastructure for high-risk categories

The CoinPay platform is built specifically for the architecture described in this guide: non-custodial, multi-chain, with developer-grade API access and a checkout layer that doesn't require category approval. For peptide merchants, that means:

- No underwriting review or MCC classification. The gateway doesn't make a business-risk judgment about your category.

- Funds flow directly to wallets you control. There's no custodial relationship that can be terminated.

- Stablecoin settlement paths for merchants who can't hold volatility exposure.

- Escrow and reputation tooling for merchants building customer trust without card-based protections.

- Webhook infrastructure built for production: retry logic, confirmation depth configuration, and order state tracking.

If you're building against the API or evaluating options, the CoinPay blog covers ongoing technical updates, and the team is reachable through the contact page for integration-specific questions.

The peptide merchant account problem is a structural problem, not a vendor problem. Crypto infrastructure doesn't solve every challenge in running a high-risk business — product compliance, customer trust, and operational resilience all still require work. What it does solve is the specific, repeatable failure of having your payment layer terminated by a third party's policy decision. That's a meaningful architectural improvement, and in 2026, it's production-ready infrastructure, not an experiment.

Try coinpayportal.com

CoinPayPortal is a non-custodial crypto payment gateway built for developers and merchants who need payment infrastructure that doesn't depend on acquiring bank relationships. Start accepting crypto payments without underwriting reviews, MCC classifications, or custodial risk.

Try CoinPay

Non-custodial crypto payments — multi-chain, Lightning-ready, and fast to integrate.

Get started →