Crypto Transactions in Production: A Payment Architecture Guide for Developers and Merchants

A customer pays. The block explorer shows a transfer. Your checkout page still says pending. Support gets a ticket. Finance asks why the order is not in the settlement report.

This is where crypto transactions stop being a blockchain concept and become an operations problem.

Teams think the problem is accepting crypto transactions. The real problem is turning unpredictable network events into a reliable merchant payment workflow: invoice state, confirmation policy, retries, reconciliation, custody boundaries, settlement, refunds, and support evidence.

That changes the conversation. You are not just integrating a wallet or listening for deposits. You are designing a payment system where the UI, blockchain, backend, accounting, and merchant dashboard must agree often enough to run a real business.

Table of contents

- Why crypto transactions fail in production

- Model crypto transactions as payment state

- Confirmation policy for crypto transactions

- Wallets, custody, and address strategy

- Webhooks, retries, and idempotency

- Reconciliation and settlement

- Escrow, disputes, and merchant trust

- Common failure modes in crypto transactions

- Implementation workflow for developers

- Where coinpayportal.com fits

Why crypto transactions fail in production

Crypto transactions look simple in demos because the demo usually ends at “payment detected.” In production, that is the beginning of the hard part.

A real merchant system has to answer questions the blockchain does not answer by itself: Which invoice does this payment belong to? Is the amount still valid after exchange-rate movement? Is the order safe to fulfill? What if the customer paid from an exchange that batched withdrawals? What if the transaction confirms after the invoice expired?

The invoice is not the system

The mistake teams make is treating the checkout invoice as the payment system. The invoice is only the customer-facing contract: pay this amount, to this destination, before this time.

The actual system includes:

- invoice creation and price locking;

- address or payment request generation;

- transaction detection;

- confirmation tracking;

- webhook delivery;

- order fulfillment rules;

- merchant ledger entries;

- settlement and withdrawal reporting;

- refund and dispute workflows.

If any of those parts are implicit, they will eventually be handled manually by support. That is not a technical edge case. It becomes the business process.

The chain is not your only source of truth

Blockchains are excellent at proving that a transfer happened. They are not designed to know your order ID, customer session, refund policy, inventory state, tax treatment, or merchant settlement cutoff.

A useful way to think about it is this: the blockchain is an evidence layer. Your payment platform is the state layer.

Practical rule: never let a block explorer be the only way your team explains whether an order was paid.

For broader payment gateway setup decisions, custody boundaries and merchant workflows are covered in this related architecture guide on crypto payment gateway setup. The same principle applies here: the API call is not the architecture.

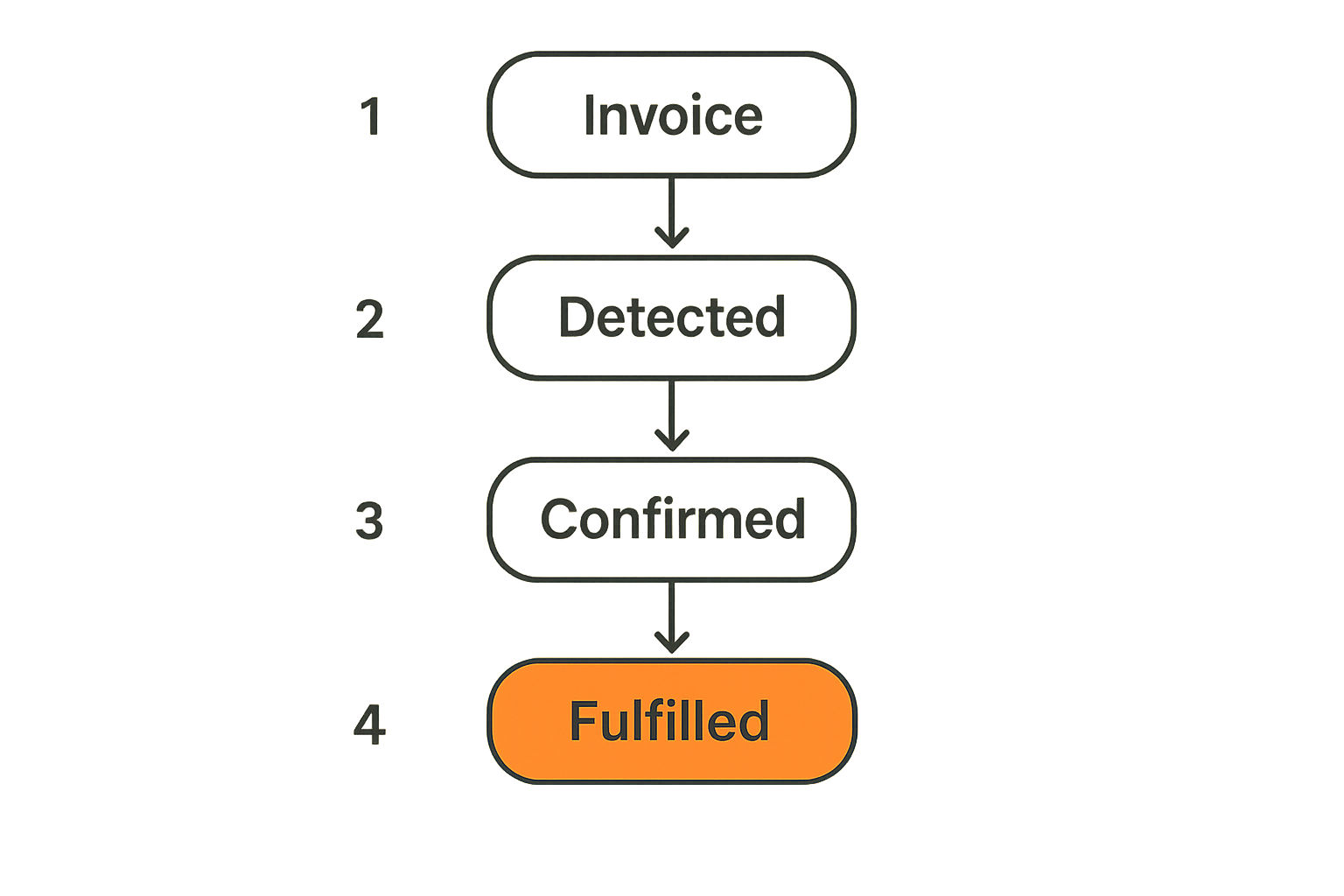

Model crypto transactions as payment state

The practical question is not “did a transaction happen?” It is “what state is the payment in, and what is the next safe action?”

That framing prevents a long list of production bugs. Instead of scattering logic across checkout pages, webhook handlers, admin dashboards, and fulfillment jobs, you define a state machine and force every component to respect it.

Use a state machine, not boolean flags

Boolean flags like paid=true, confirmed=false, and expired=true become contradictory under pressure. A late payment can be both expired and paid. A partial payment can be detected but not fulfillable. An overpayment can be confirmed but require a refund decision.

A more useful transaction model looks like this:

| State | Meaning | Typical next action |

|---|---|---|

created | Invoice exists, no transaction detected | Show payment instructions |

detected | Network transaction seen | Wait for confirmations |

confirming | Transaction has confirmations but not enough | Keep monitoring |

paid | Payment meets amount and confirmation policy | Fulfill order or notify merchant |

underpaid | Amount received is below required threshold | Ask customer to top up or support review |

overpaid | Amount exceeds expected value | Fulfill and create refund workflow if needed |

expired | Payment window passed with no acceptable payment | Cancel or require new invoice |

late_paid | Payment arrived after expiration | Manual or automated exception handling |

refunded | Funds returned or offset | Close financial loop |

This table is not universal. Your thresholds and names may differ. The point is that every state should have one owner, one meaning, and one next action.

Separate customer-visible and operator-visible states

Customers need simple language: waiting for payment, payment received, confirming, complete, issue detected.

Operators need more detail: transaction hash, chain, address, confirmation count, expected amount, received amount, FX rate, invoice expiry, webhook attempts, fulfillment status, and settlement batch.

What breaks in practice is exposing internal uncertainty directly to customers or hiding operational detail from support. Both create tickets. One creates panic; the other creates blind debugging.

Related reading from our network: teams building publishing pipelines face a similar state-management problem when automation needs approval gates, as discussed in this guide to AI blog publishing software workflow architecture. Different domain, same lesson: workflow state beats scattered automation.

Confirmation policy for crypto transactions

Not all crypto transactions should be treated the same. A low-value stablecoin payment on a fast network may need a different policy than a high-value payment on a slower chain. A marketplace payout has different risk than a digital download.

The mistake teams make is hardcoding one confirmation rule and pretending it is a security model.

Risk should drive confirmation depth

Confirmation policy should depend on at least four factors:

- asset and network behavior;

- payment value;

- product or service reversibility;

- merchant risk tolerance.

For example, a small payment for a low-risk digital feature may be fulfilled after a lighter confirmation policy. A high-value physical shipment may require deeper confirmation and manual review if anything looks unusual.

Practical rule: confirmation depth is a business risk control, not just a blockchain setting.

Avoid burying this policy in a webhook handler. Store it with the invoice or merchant configuration so support and finance can explain why one transaction was fulfilled faster than another.

Handle late, partial, and overpaid transactions

The happy path is exact amount, correct chain, before expiration, enough confirmations. Production systems must handle the rest.

Common exceptions include:

- customer sends the right asset after the invoice expires;

- customer sends less than the requested amount because of exchange withdrawal fees;

- customer sends more than required;

- customer pays on the wrong network;

- transaction is detected but never reaches the required confirmation depth;

- customer sends from a custodial exchange that delays or batches withdrawals.

Do not force every exception into “failed.” That loses information. A late confirmed payment is not the same as no payment. An underpayment is not the same as fraud. These distinctions matter for refunds, customer support, accounting, and merchant reputation.

Wallets, custody, and address strategy

Wallet architecture determines what your payment system can prove, automate, and recover from. It also defines who carries operational risk.

Teams often start with “we need an address.” The practical question is: who controls the private keys, who can move funds, how are addresses mapped to invoices, and how does finance audit the flow later?

Decide who controls funds before you write code

Custody is not a UI preference. It changes security responsibilities, compliance posture, refund workflows, and incident response.

A simple comparison:

| Model | Funds controlled by | Benefits | Tradeoffs |

|---|---|---|---|

| Non-custodial merchant wallet | Merchant | Strong merchant control, reduced platform custody risk | Merchant must manage keys and withdrawals |

| Gateway-managed custody | Payment provider | Easier settlement and refunds | Higher trust and compliance burden |

| Escrow wallet | Conditional release logic | Better marketplace trust and dispute handling | More complex lifecycle and support rules |

For merchants, non-custodial flows can be attractive because the payment provider does not need to hold funds indefinitely. For marketplaces, escrow can be useful when delivery, release, and dispute timing matter.

Generate addresses with auditability in mind

Address reuse creates privacy and reconciliation problems. One address per invoice is cleaner because it gives you a direct mapping between expected payment and observed transaction.

At minimum, store:

- generated address or payment request;

- derivation path or address metadata, where applicable;

- invoice ID and merchant ID;

- asset and network;

- expected amount;

- expiration timestamp;

- transaction hashes observed for that invoice.

Do not rely on “we can search the chain later.” You can, but it is slower, noisier, and often ambiguous when exchanges batch payments.

Webhooks, retries, and idempotency

Webhooks are where clean payment architecture often gets damaged. A webhook arrives twice. Your server times out. The order gets fulfilled twice. Or the webhook fails once, and the merchant never sees the payment.

The mistake teams make is assuming webhooks are delivery guarantees. They are messages over unreliable networks. Design accordingly.

Treat webhooks as hints, not final truth

A webhook should tell your system that something changed. Your system should then verify the current payment state before taking irreversible action.

For example:

{

"event": "payment.confirmed",

"invoice_id": "inv_92f4",

"transaction_id": "tx_7a31",

"asset": "USDT",

"network": "polygon",

"confirmations": 64,

"status": "paid"

}

When this arrives, the merchant backend should check whether inv_92f4 is already fulfilled, whether the amount matches, and whether the event signature is valid. If the order is already complete, acknowledge the webhook and do nothing.

Related reading from our network: if your acquisition stack depends on structured content being discoverable by automated systems, this piece on answer AI architecture for AI answer engines is a useful adjacent read. In both cases, machine-readable structure matters because downstream systems will consume it without human context.

Make every payment update idempotent

Idempotency means the same update can be processed multiple times without changing the final result incorrectly. In payments, it is not optional.

Use stable identifiers:

- invoice ID for the merchant order;

- transaction hash for the blockchain event;

- event ID for webhook delivery;

- settlement batch ID for finance reporting.

A simple rule: fulfillment should be keyed by invoice state transition, not by webhook receipt.

Practical rule: a webhook can trigger a check, but it should not be the only reason inventory ships or access is granted.

For implementation details and API behavior, developers should keep the CoinPay documentation close while designing webhook verification, event retries, and merchant-side state updates.

Reconciliation and settlement

Reconciliation is usually treated as a finance task that happens after payment. That is too late. Reconciliation starts when the invoice is created, because that is when you define what should be true later.

If your system cannot connect invoice, transaction, order, ledger entry, and settlement record, finance will build that connection manually in spreadsheets.

Reconciliation starts at invoice creation

Every invoice should carry enough metadata to reconcile without guessing:

- merchant ID;

- order ID;

- customer reference, if appropriate;

- asset and network;

- expected crypto amount;

- fiat reference amount;

- exchange-rate timestamp;

- destination address;

- expiry time;

- confirmation policy;

- fees, if known;

- settlement destination.

The practical question is whether someone can answer this later: “Which customer order produced this on-chain transaction and which settlement included it?”

If the answer requires reading logs from three services, the system is not ready.

Settlement is an operational contract

Settlement is not just moving funds. It is the agreement between the payment system and the merchant about timing, fees, reporting, and finality.

Define these rules explicitly:

| Settlement rule | Why it matters |

|---|---|

| Cutoff time | Determines which payments appear in each report |

| Fee treatment | Prevents merchant balance disputes |

| Asset conversion | Clarifies FX exposure and accounting values |

| Withdrawal minimums | Avoids dust and uneconomic transfers |

| Failed withdrawal handling | Keeps payout issues from becoming silent losses |

| Report format | Lets finance import data reliably |

What breaks in practice is treating settlement as a wallet withdrawal button. Merchants need a ledger they can trust, not just a balance number.

Escrow, disputes, and merchant trust

Some crypto transactions are straightforward: customer pays, merchant delivers, transaction complete. Marketplaces and higher-risk commerce are different.

If delivery happens later, or if buyer and seller do not fully trust each other, escrow can turn a one-step payment into a controlled lifecycle.

Escrow changes the transaction lifecycle

Escrow adds states such as funded, in review, released, disputed, partially released, refunded, and expired. That complexity is useful only if the business process needs it.

Use escrow when:

- buyer and seller are different parties;

- delivery takes time;

- dispute resolution is part of the value proposition;

- funds should not be released immediately;

- reputation or milestone completion affects payout.

Do not add escrow because it sounds safer. Add it because the transaction workflow needs conditional release.

For marketplace-style flows, CoinPay escrow is relevant when funds need to be held until delivery conditions, dispute windows, or release approvals are satisfied.

Dispute evidence must be designed early

Dispute handling fails when evidence is scattered. If the only proof you have is a transaction hash, you can prove payment happened, but not whether the seller delivered or the buyer accepted.

Capture evidence at each step:

- invoice terms shown to the buyer;

- payment transaction and confirmation history;

- merchant fulfillment event;

- delivery or access logs;

- buyer approval or complaint;

- support notes and resolution outcome.

Related reading from our network: gig and marketplace teams run into similar workflow problems around screening, verification, and status tracking; this guide to Indeed part time jobs AI-assisted workflow is a loose but useful comparison for thinking about multi-step trust processes.

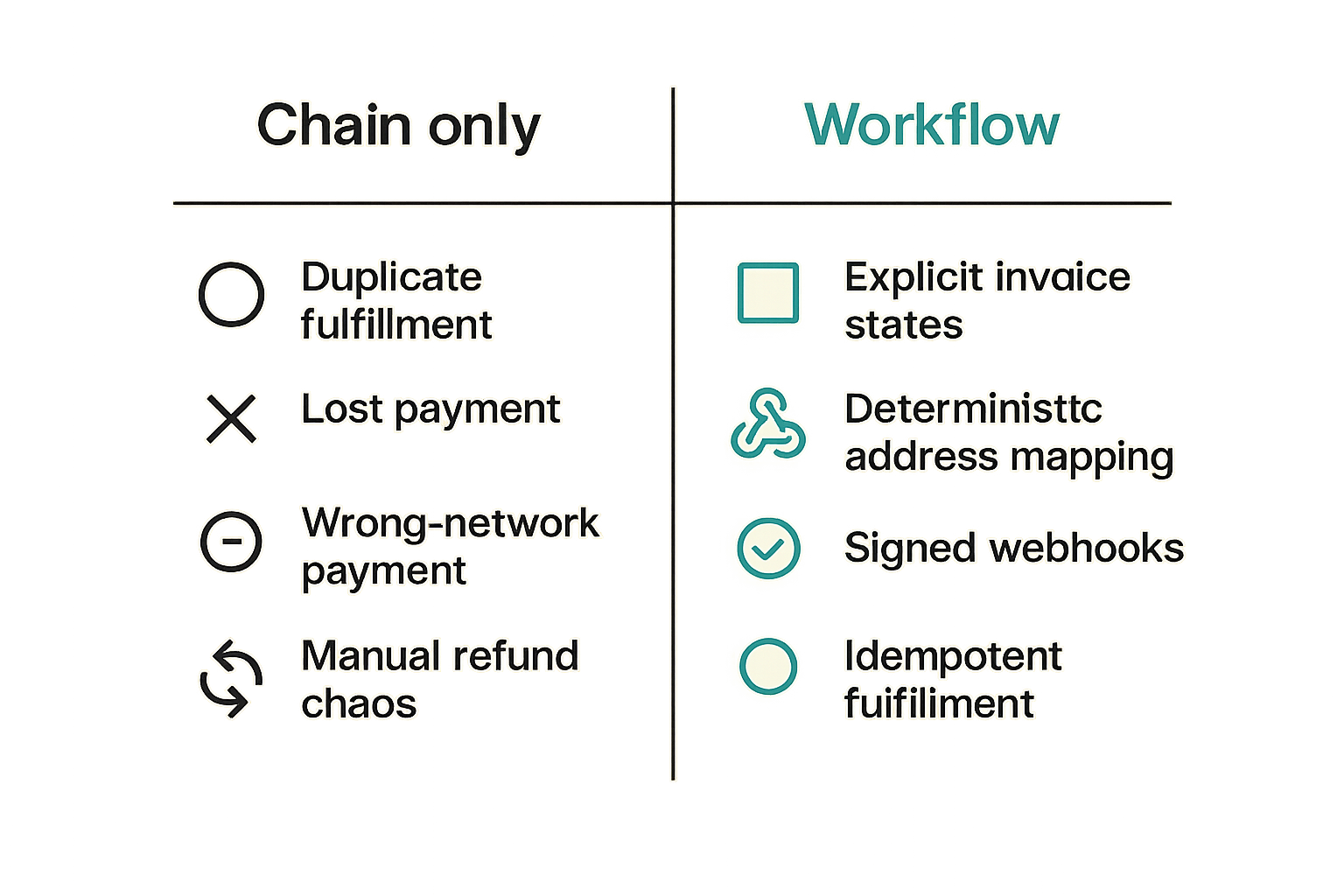

Common failure modes in crypto transactions

Most production failures are not exotic blockchain attacks. They are ordinary workflow mismatches.

The chain says one thing, the checkout says another, the merchant dashboard says a third, and support has to guess which one is right.

What fails when teams only watch the chain

Watching the chain is necessary. It is not sufficient.

Common failure modes include:

- Duplicate fulfillment: webhook retry triggers the same order twice.

- Lost payment: customer pays after invoice expiration, but the system stops monitoring.

- Wrong-network payment: customer sends the right token on a network the merchant does not support.

- Ambiguous batch payment: exchange withdrawal does not map cleanly to one invoice.

- Manual refund chaos: overpayments are handled in chat without ledger entries.

- Support blind spots: customer provides a hash, but support cannot connect it to an order.

- Finance mismatch: settlement report totals do not match detected transactions.

These are architecture failures, not customer education failures.

What works in production

Production systems tend to be boring in the right ways.

They have:

- explicit invoice states;

- deterministic address mapping;

- confirmation policies stored with the invoice;

- signed webhooks and retries;

- idempotent fulfillment;

- searchable transaction records;

- exception queues for underpaid, overpaid, late, and wrong-network payments;

- settlement reports that match ledger entries.

Practical rule: if support cannot resolve a payment issue from your internal dashboard, your architecture is incomplete.

The goal is not to remove every exception. The goal is to make exceptions visible, classified, and recoverable.

Implementation workflow for developers

A good crypto payment integration is built from the state model outward. Do not start with the checkout button. Start with the payment lifecycle and the data you need to prove each transition.

A practical build sequence

Use this sequence when implementing crypto transactions for a merchant product, SaaS platform, or marketplace:

- Define supported assets and networks. Decide what you actually support, and reject everything else clearly.

- Create the invoice model. Store merchant, order, amount, asset, network, expiry, and confirmation policy.

- Generate a unique payment destination. Prefer one address or payment request per invoice where possible.

- Monitor blockchain events. Detect incoming transactions and associate them to invoices.

- Apply confirmation policy. Move from detected to confirming to paid only when rules are met.

- Deliver signed webhooks. Notify merchant systems, but allow retry and verification.

- Make fulfillment idempotent. Fulfill once per successful invoice transition.

- Record ledger entries. Track expected amount, received amount, fees, adjustments, and settlement status.

- Build exception queues. Surface late, partial, overpaid, and unsupported-network payments.

- Generate settlement reports. Let merchants reconcile orders, transactions, fees, and payouts.

This order matters. If you bolt reconciliation on later, you will usually discover that the data you need was never stored.

Minimal transaction record schema

Your schema will vary, but a practical starting point looks like this:

CREATE TABLE crypto_payment_transactions (

id UUID PRIMARY KEY,

merchant_id UUID NOT NULL,

invoice_id UUID NOT NULL,

order_id TEXT,

asset TEXT NOT NULL,

network TEXT NOT NULL,

destination_address TEXT NOT NULL,

expected_amount NUMERIC(36, 18) NOT NULL,

received_amount NUMERIC(36, 18),

fiat_reference_amount NUMERIC(18, 2),

fiat_currency TEXT,

rate_locked_at TIMESTAMP,

invoice_expires_at TIMESTAMP NOT NULL,

tx_hash TEXT,

confirmations INTEGER DEFAULT 0,

status TEXT NOT NULL,

confirmation_policy JSONB NOT NULL,

webhook_delivery_count INTEGER DEFAULT 0,

settlement_batch_id UUID,

created_at TIMESTAMP NOT NULL,

updated_at TIMESTAMP NOT NULL

);

CREATE UNIQUE INDEX uniq_invoice_tx

ON crypto_payment_transactions(invoice_id, tx_hash);

Two details matter here. First, amounts need precision. Do not use floating-point types for payment amounts. Second, the unique index helps prevent duplicate transaction handling when the same event is processed more than once.

Where coinpayportal.com fits

Crypto transactions become manageable when the payment infrastructure owns the repetitive workflow: invoice creation, payment detection, confirmation state, webhook delivery, escrow where needed, and merchant reporting.

The job of infrastructure is not to hide the blockchain. It is to translate blockchain activity into merchant actions that are consistent, auditable, and supportable.

Use infrastructure to enforce payment rules

If every merchant implementation writes its own confirmation logic, webhook retry logic, exception handling, and settlement reporting, every merchant also inherits the same failure modes.

A payment layer should enforce the boring rules:

- validate supported networks;

- bind invoices to payment destinations;

- track crypto transactions through confirmation states;

- retry webhooks safely;

- expose exceptions clearly;

- preserve settlement and reconciliation metadata.

That is where infrastructure earns its place. It reduces the amount of custom payment logic developers have to maintain while keeping merchants close to the actual transaction evidence.

Keep the merchant workflow visible

Merchants do not need a black box. They need a system that shows what happened, what state the payment is in, and what action is safe next.

For developers and merchants building crypto payment infrastructure, coinpayportal.com focuses on the practical layer: checkout, non-custodial payment flows, escrow, webhooks, and merchant-side operations. The point is not to make crypto transactions look magical. The point is to make them operational.

Try coinpayportal.com

coinpayportal.com is for developers and merchants building crypto payment infrastructure. Start with Try coinpayportal.com and build crypto transactions as a real payment workflow, not a block explorer lookup.

Try CoinPay

Non-custodial crypto payments — multi-chain, Lightning-ready, and fast to integrate.

Get started →