Crypto Merchant Account Architecture: A Practical 2026 Guide for Developers and Merchants

A crypto merchant account looks simple until the first production order gets stuck between checkout, chain confirmation, settlement, and support.

Teams think the problem is accepting a coin. The real problem is operating a payment workflow where state lives in multiple places: your cart, your backend, the gateway, the blockchain, the merchant ledger, and the customer inbox.

That changes the conversation. A crypto merchant account is not just a wallet address, a hosted checkout page, or a dashboard. It is the operational layer that decides how invoices are created, how payments are detected, how risk is handled, how funds settle, and how finance proves what happened later.

The practical question is not whether crypto payments can work. They can. The question is whether your account model, API design, webhook handling, custody boundary, and reconciliation process survive real customers, network congestion, retries, underpayments, refunds, and support tickets in 2026.

Table of contents

- What a crypto merchant account really has to operate

- Crypto merchant account architecture in 2026

- Account models compared: custodial, non-custodial, and hybrid

- The checkout workflow that actually matters

- Settlement, reconciliation, and accounting

- Trust, risk, and merchant controls

- Developer implementation sequence

- Common failure modes in production

- How to evaluate a crypto merchant account provider

- Where coinpayportal.com fits

What a crypto merchant account really has to operate

A crypto merchant account is the commercial and technical container for accepting cryptocurrency payments. But that definition is too thin to be useful. In production, the account is where payment rules, merchant identity, supported assets, webhook credentials, settlement settings, refund workflows, and reporting boundaries meet.

Merchant account versus checkout button

The mistake teams make is treating a crypto merchant account as a checkout widget. A widget can collect intent. It cannot, by itself, answer operational questions:

- Which asset and network was used?

- What exchange rate was shown to the buyer?

- Did the buyer pay before the invoice expired?

- Was the payment underpaid, overpaid, duplicated, or delayed?

- Who owns the private keys or settlement address?

- Which internal order should finance recognize?

- What should support say when the transaction is pending?

A checkout button is an interface. A merchant account is the workflow behind it. If you only design the interface, the unresolved complexity moves into support and finance.

Practical rule: Treat the crypto merchant account as a payment operating system, not as a wallet address with a nicer UI.

Why the account is a state machine

A useful way to think about it is as a state machine with external dependencies. Your customer sees a price and sends funds. Your backend sees an order. The chain sees a transaction. The gateway sees an invoice. Finance sees a receivable. These states do not update at the same time.

Common states include:

invoice_createdpayment_detectedpartially_paidconfirmedexpiredsettledrefundedmanual_review

The account must define transitions between those states. Without that, teams end up writing one-off exception logic for every failed checkout. If you are still choosing a gateway, the broader crypto payment gateway setup workflow is worth reviewing because the merchant account sits inside that architecture.

Crypto merchant account architecture in 2026

The practical architecture has three layers: custody, pricing, and operations. If those are clear, the rest of the integration becomes easier. If they are vague, every later decision becomes political.

Custody boundary

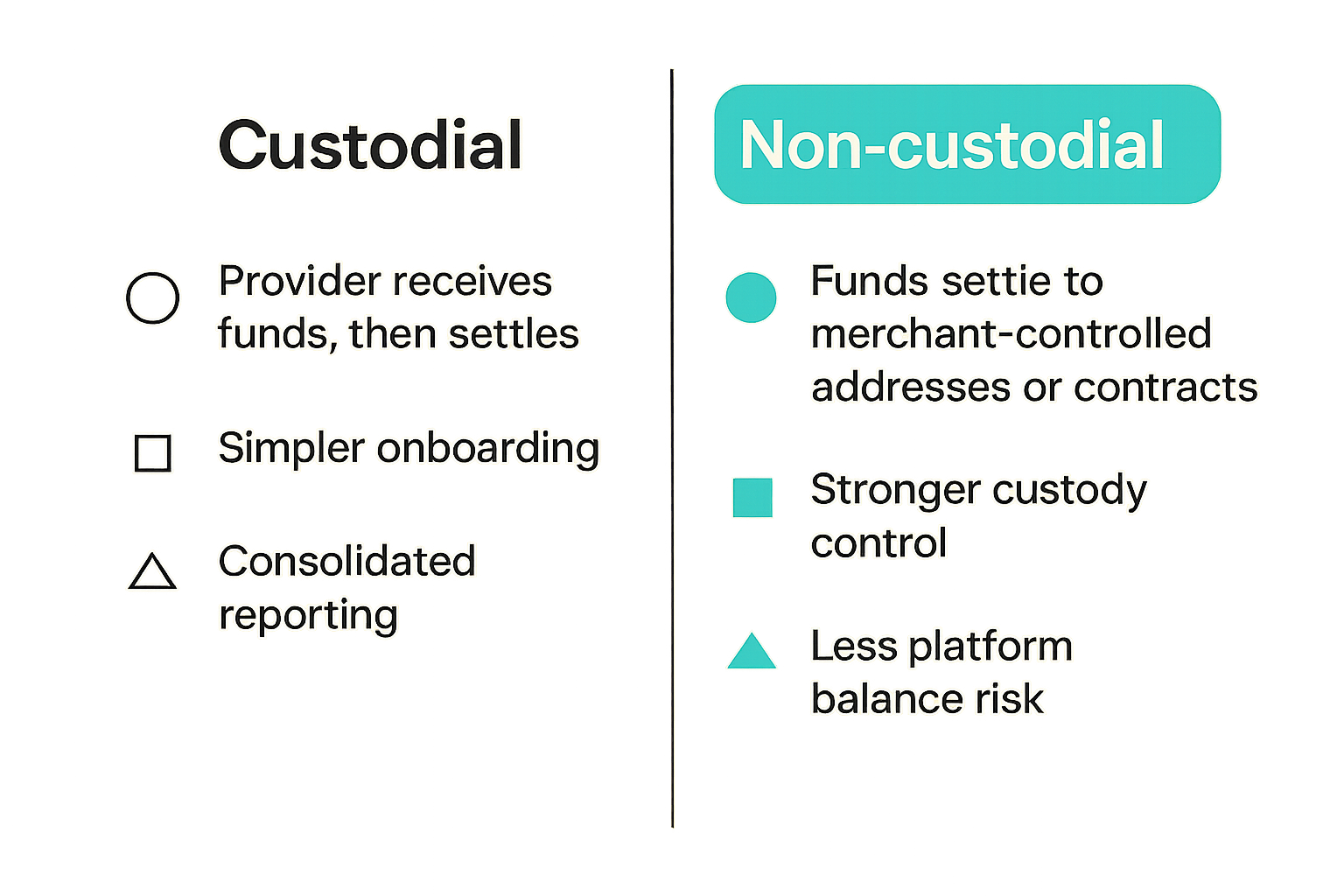

Custody is the first architecture decision. Who can move the funds after the buyer pays?

In a custodial model, the provider receives funds and later settles to the merchant. This can simplify reporting and fiat conversion, but it introduces platform risk, withdrawal rules, and potentially more compliance obligations.

In a non-custodial model, payments move to merchant-controlled wallets or smart-contract-controlled flows. This reduces reliance on the provider holding funds, but it makes key management, wallet operations, refunds, and accounting more explicit.

Hybrid models exist. A marketplace may use escrow for a portion of the flow while sending direct settlement for ordinary invoices. A SaaS vendor may accept stablecoins non-custodially but use a processor for card fallback.

Practical rule: Decide custody before you design checkout. Custody determines settlement, refunds, support language, and risk ownership.

Pricing and network selection

The second decision is how the account prices orders. Crypto payments are not just asset choices. They are asset plus network plus confirmation policy plus expiration window.

A USDC payment on Ethereum mainnet behaves differently from USDC on a low-cost chain. Bitcoin behaves differently from Lightning. Volatile assets behave differently from stablecoins. The account needs rules for supported combinations, not a generic crypto accepted claim.

Merchant settings should answer:

- Which assets are accepted?

- Which networks are enabled for each asset?

- How long is a quote valid?

- Is the merchant pricing in fiat, crypto, or both?

- What happens if the buyer sends after expiration?

- Is overpayment credited, refunded, or reviewed?

Related reading from our network: teams handling structured data face a similar integrity problem when fields drift away from source truth, and the workflow in Schema Def in 2026 is a useful parallel for keeping machine-readable payment data trustworthy.

Merchant operations plane

The third layer is the operations plane. This is the part many early integrations skip.

A merchant operations plane includes:

- API keys and webhook signing secrets

- Invoice and payment search

- Settlement exports

- Refund tooling

- Manual review queues

- Role-based access

- Customer-facing status pages or receipt links

- Audit logs for finance and support

What breaks in practice is not usually the happy path. It is the missing dashboard action when an order is paid late, the missing export column finance needs, or the missing support note explaining why an invoice moved to manual review.

Account models compared: custodial, non-custodial, and hybrid

A crypto merchant account should match your business model. A marketplace, a digital goods seller, a SaaS subscription business, and a high-ticket B2B invoice flow do not need the same payment posture.

Comparison table

| Model | How funds move | Strengths | Tradeoffs | Best fit |

|---|---|---|---|---|

| Custodial | Provider receives funds, then settles | Simpler onboarding, consolidated reporting, possible fiat conversion | Provider risk, withdrawal policies, more dependency on platform controls | Merchants prioritizing simplicity and managed operations |

| Non-custodial | Funds settle to merchant-controlled addresses or contracts | Stronger custody control, less platform balance risk, clearer ownership | More responsibility for wallets, refunds, keys, and reconciliation | Developers, crypto-native merchants, marketplaces with internal ops |

| Hybrid | Some flows are direct, some use escrow or managed settlement | Flexible risk handling, useful for marketplaces and high-value orders | More state transitions, more complex support and accounting | Platforms that need both speed and conditional release |

The table is not a moral ranking. It is an operating model choice. The wrong model creates work later.

When each model fails

Custodial models fail when merchants cannot tolerate delayed withdrawals, platform balance exposure, or opaque settlement timing. Non-custodial models fail when the merchant is not ready to manage wallets, support policies, or transaction-level accounting. Hybrid models fail when product teams add conditions faster than engineering can encode and support can explain.

The mistake teams make is picking the model based on checkout conversion alone. Conversion matters, but the payment account also touches finance close, dispute handling, treasury, support, and compliance review.

Practical rule: Choose the account model that your operations team can explain on a bad day, not only the one your checkout team likes on a demo day.

The checkout workflow that actually matters

The checkout page is visible. The workflow behind it is where reliability lives. A crypto merchant account needs a deterministic path from cart to invoice to chain transaction to order fulfillment.

Invoice creation

Invoice creation should be server-side. The frontend can request a checkout, but your backend should create the order, call the provider, persist the invoice ID, and return the payment instructions.

A typical invoice object should store:

- Internal order ID

- Provider invoice ID

- Customer ID or session ID

- Fiat amount and currency

- Crypto amount and asset

- Network

- Quote timestamp

- Expiration timestamp

- Destination address or payment request

- Current payment state

Do not rely on the browser as the source of truth. Users close tabs, mobile wallets interrupt sessions, and checkout redirects fail.

Payment detection and confirmation policy

Detection and confirmation are not the same. Detection means the network has seen a transaction that may satisfy the invoice. Confirmation means your policy considers it final enough for the business action.

For low-value digital goods, you may accept faster confirmation. For high-value physical goods, you may require more confirmations or manual review. For stablecoins on fast networks, the policy may be different again.

The account should let you define confirmation thresholds per asset, network, amount, and product risk. If it cannot, your application will need to implement risk exceptions itself.

Webhooks, idempotency, and retries

Webhooks are the backbone of the crypto merchant account integration. They are also where many systems fail.

A webhook handler must be idempotent. It should tolerate duplicate delivery, out-of-order delivery, network retries, and events arriving after the customer has left the page. It should verify signatures, store raw events, and update order state only through allowed transitions.

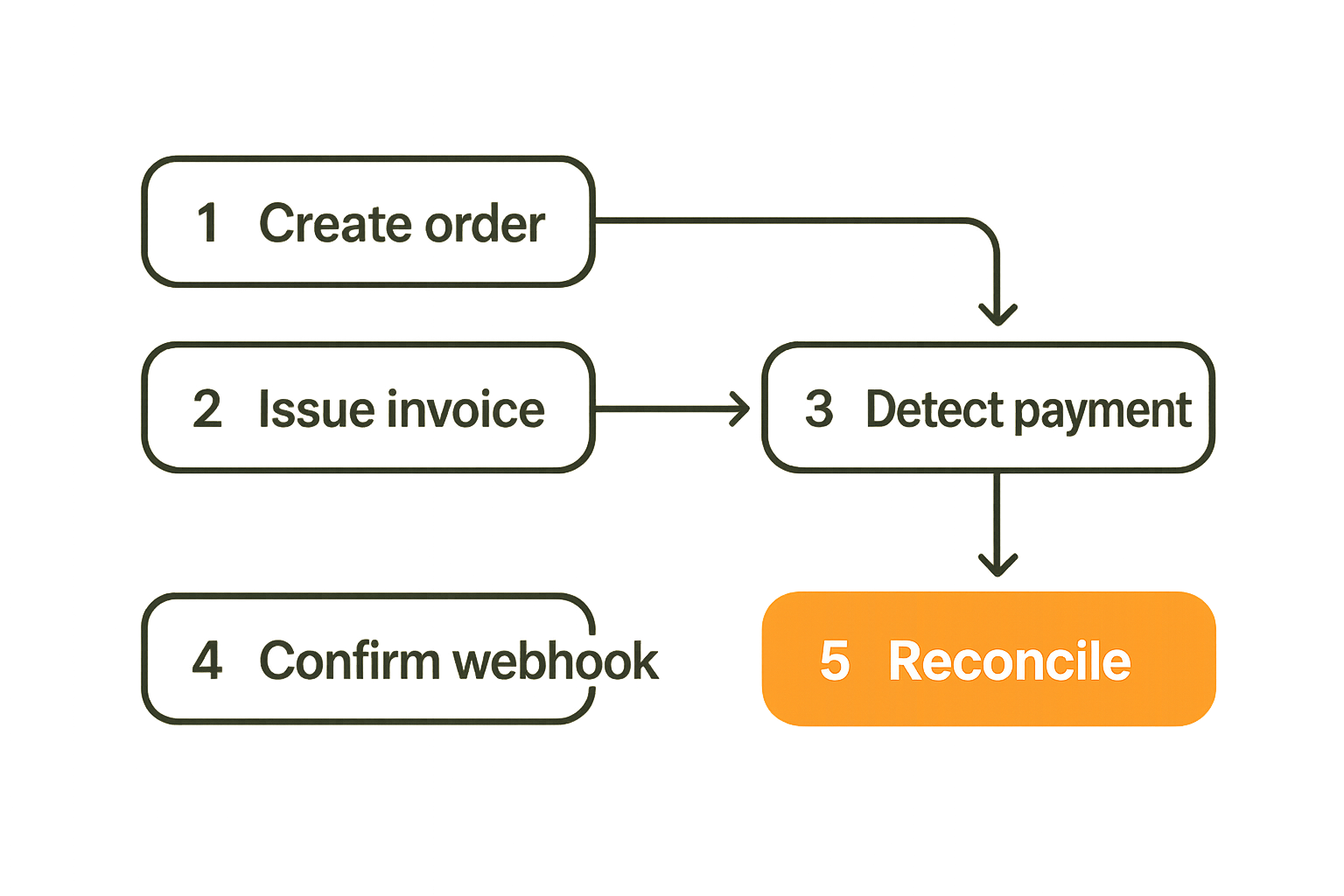

A safe flow looks like this:

- Customer starts checkout.

- Backend creates an internal order in

pending_payment. - Backend creates provider invoice and stores provider ID.

- Customer sends payment.

- Provider detects transaction and sends webhook.

- Backend verifies signature and stores event.

- Backend checks current order state and applies allowed transition.

- Fulfillment runs only after the required confirmation state.

- Settlement and reconciliation jobs run independently of checkout.

If you are implementing against an API, start with the provider reference material, then write integration tests against your own state transitions. CoinPay documentation for developers is available in the CoinPay docs, but your application still needs its own order-state rules.

Settlement, reconciliation, and accounting

A payment is not done when the customer sends crypto. It is done when the merchant can prove what was received, where it went, how it maps to an order, and whether any exceptions remain open.

Order state versus blockchain state

Order state is business state. Blockchain state is network state. They overlap, but they are not identical.

For example, a transaction may be confirmed on-chain but still require manual review because it was underpaid. An order may be canceled in your system while a late transaction arrives on-chain. A payment may satisfy the invoice but settle to a wallet that finance has not yet mapped to an entity.

This is why reconciliation should not be an afterthought. Your ledger should join provider invoice records, chain transaction hashes, internal order IDs, settlement addresses, amounts, fees, and timestamps.

The reconciliation ledger

The reconciliation ledger does not need to be complex at the start, but it must be explicit. At minimum, store:

order_idinvoice_idassetnetworkexpected_amountreceived_amounttx_hashconfirmation_statusfee_amountsettlement_addressrecognized_revenue_statusexception_reason

Finance will eventually ask questions that the checkout page cannot answer. Which invoices expired but later received funds? Which orders were fulfilled before final confirmation? Which payments were refunded? Which network fees reduced net settlement?

Refunds, disputes, and chargeback expectations

Crypto does not have card-network chargebacks in the same way card payments do. That does not mean there are no disputes. Customers still send the wrong amount, use the wrong network, claim non-delivery, mistype addresses, or ask for refunds.

Your crypto merchant account should define refund policy in plain operational terms:

- Can support issue refunds from the dashboard?

- Are refunds sent in the same asset or fiat equivalent?

- Who approves high-value refunds?

- What address is used for refunds?

- How do you handle chain fees?

- What happens if the customer sent from an exchange deposit address?

The absence of chargebacks shifts work from card-network dispute rails to merchant support, policy, and audit trails. That is not automatically better or worse. It is different.

Trust, risk, and merchant controls

Payments are trust infrastructure. Crypto rails change the mechanics, but they do not remove the need for controls. The merchant account should make risk decisions visible and configurable.

Escrow, reputation, and marketplaces

Marketplaces have a different problem from single-seller stores. The buyer may trust the platform but not the seller. The seller may want proof that the buyer has paid before shipping. The platform may need conditional release.

That is where escrow and reputation become account-level capabilities, not add-ons. A marketplace payment may need states such as funded, awaiting delivery, release requested, disputed, released, and refunded. If your business needs conditional release, evaluate escrow early rather than patching it into an ordinary checkout later. CoinPay offers an escrow payment flow for use cases where release conditions matter.

Fraud, abuse, and sanctions screening

Crypto merchant accounts should also support basic controls against abuse. The exact requirements depend on jurisdiction, product category, customer type, and risk appetite, but ignoring the problem is not an architecture.

Practical controls may include:

- Transaction monitoring thresholds

- Manual review for high-value orders

- Blocked assets or networks

- Wallet risk flags from external providers

- Country or product restrictions

- Velocity limits on account activity

- Audit logs for admin actions

Do not bury these decisions inside scattered application code. Put them near the payment state machine where support, finance, and compliance can reason about them.

Support readiness

Support needs more than a transaction hash. They need a narrative that maps technical state to customer language.

Good support tooling answers:

- Did we generate an invoice?

- Did the customer send funds?

- Was the amount correct?

- Is the transaction confirmed?

- Is fulfillment blocked by policy?

- Is a refund possible?

- What should we tell the customer now?

Related reading from our network: Product Iteration Best Practices makes a similar point for software teams: signals only matter when they feed an operating loop, not when they sit in disconnected tools.

Developer implementation sequence

A crypto merchant account integration should be built in boring layers. Boring is good. Boring means failures are isolated and support can inspect state.

Minimal production path

Start with the smallest reliable path before adding assets, subscriptions, escrow, discounts, or marketplace splits.

- Define accepted assets and networks.

- Decide custody and settlement addresses.

- Create internal order states and allowed transitions.

- Implement server-side invoice creation.

- Store invoice IDs and payment instructions.

- Verify signed webhooks.

- Make webhook handling idempotent.

- Gate fulfillment on confirmation policy.

- Build reconciliation exports.

- Create support views for exceptions.

- Test late, partial, duplicate, and wrong-network payments.

- Roll out to limited traffic before enabling broadly.

This sequence is intentionally operational. If you cannot reconcile a test order, you are not ready to accept production payments.

Example webhook handler

The details vary by provider, but the pattern should look familiar:

async function handlePaymentWebhook(req, res) {

const event = verifySignature(req.body, req.headers['x-signature'])

await db.webhookEvents.insert({

provider_event_id: event.id,

invoice_id: event.invoice_id,

type: event.type,

raw_payload: req.body,

received_at: new Date()

}).catch(ignoreDuplicateEvent)

const order = await db.orders.findByInvoiceId(event.invoice_id)

if (!order) return res.status(202).send('unknown invoice stored')

const nextState = transition(order.payment_state, event.type)

if (!nextState) return res.status(200).send('no transition')

await db.orders.update(order.id, {

payment_state: nextState,

last_payment_event_id: event.id

})

if (nextState === 'confirmed') {

await enqueueFulfillment(order.id)

}

return res.status(200).send('ok')

}

The important part is not the syntax. It is the separation of concerns: verify, store, transition, fulfill. Do not mix all of that into a controller that also renders checkout.

Testing before mainnet

Test the failure cases before you test the marketing page.

Use cases to simulate:

- Exact payment before expiration

- Payment after expiration

- Partial payment

- Overpayment

- Duplicate webhook

- Webhook arriving before redirect return

- Wrong asset or network

- Chain confirmation delay

- Refund request

- Provider outage or API timeout

Many teams test only the happy path because the happy path is easy to demo. Production punishes that quickly.

Common failure modes in production

What breaks in practice is usually predictable. The issue is not that crypto payments are impossible. The issue is that teams under-specify the workflow.

What works

What works is a simple, explicit system:

- One source of truth for internal order state

- Provider invoice IDs stored at creation time

- Webhook events stored before processing

- Idempotent state transitions

- Clear confirmation thresholds

- Finance exports tied to transaction hashes

- Support screens that show payment history

- Manual review for ambiguous cases

This architecture does not require a large team. It requires discipline about state.

What fails

What fails is treating the chain as the database and the frontend as the workflow engine.

Failure patterns include:

- Creating invoices only in the browser

- Fulfilling orders on redirect return instead of webhook confirmation

- Not storing raw webhook payloads

- Assuming webhooks arrive once and in order

- Ignoring underpayments and late payments

- Mixing testnet and mainnet configuration

- Using one wallet address without invoice attribution

- Letting support manually change order state without audit logs

These are not edge cases. They are normal production conditions.

Edge cases teams forget

Some edge cases are boring until they cost money.

A buyer sends from an exchange that batches withdrawals, so the amount and timing do not match their expectation. A customer sends the correct asset on the wrong network. A wallet suggests a fee that delays confirmation. A user pays an expired invoice from a screenshot. A merchant changes settlement wallets while old invoices remain open.

The account needs policy for these cases. If the provider cannot represent them, your internal system must.

Related reading from our network: platforms serving freelancers and marketplaces run into similar support and trust boundaries, and Gig Work Platforms in 2026 is an adjacent look at marketplace risk, automation, and operational policy.

How to evaluate a crypto merchant account provider

Provider evaluation should not start with a logo grid of supported coins. Start with operational questions. Coins are easy to list. Payment correctness is harder.

Questions for product and finance

Ask:

- What assets and networks are actually needed by our customers?

- Do we price in fiat, crypto, or both?

- How do we handle volatility during checkout?

- What settlement schedule do we need?

- Who owns refunds?

- What reporting does finance require at month-end?

- Do we need escrow, marketplace release, or split payments?

A provider that looks good for a simple store may not work for a marketplace. A provider that works for crypto-native users may create friction for mainstream buyers.

Questions for engineering

Ask:

- Is invoice creation server-side and deterministic?

- Are webhook signatures documented and testable?

- Are events idempotent and replayable?

- Can we retrieve invoice and transaction status by API?

- Are sandbox and production environments cleanly separated?

- Are rate limits documented?

- What happens during provider downtime?

- Can we export data for reconciliation?

If the answer to webhook behavior is vague, slow down. Webhooks are where your backend meets payment truth.

Questions for support

Ask:

- Can support search by order ID, invoice ID, wallet address, or transaction hash?

- Can support see the exact payment state and reason?

- Is there an audit log for admin actions?

- Can support initiate or request refunds safely?

- Are ambiguous payments routed to review?

- Can customer messages be explained without engineering intervention?

Support tooling is part of payment architecture. If support has to ask engineering to decode every transaction hash, the account is not operationally ready.

Where coinpayportal.com fits

A crypto merchant account should reduce moving parts without hiding the parts that matter. That is the balance CoinPay focuses on: developer-friendly payment infrastructure for merchants that need real checkout, state, and operational workflows rather than crypto hype.

Non-custodial gateway posture

For many builders, the right default is to avoid unnecessary custody while still using gateway infrastructure for invoices, payment detection, and merchant operations. That keeps the custody boundary clearer while giving developers a structured integration path.

This does not remove your responsibility to design order state, reconciliation, or support workflows. It gives you a better place to anchor them. If you need a broader merchant onboarding view, the guide on how to accept crypto payments covers the business-side decisions around gateways, compliance posture, and checkout readiness.

Product fit checklist

CoinPay is a practical fit when you need:

- Crypto checkout without building payment detection from scratch

- A non-custodial posture for merchant settlement

- Escrow-style workflows for conditional release

- Developer documentation and API-oriented integration

- Merchant operations that connect checkout to support and reconciliation

- A payment layer that respects custody boundaries

It is not magic. You still need to decide policies, test edge cases, and connect payment state to fulfillment. The value is in having the account and gateway layer handle the payment-specific workflow so your team is not inventing it order by order.

Closing implementation advice

The practical way to implement a crypto merchant account in 2026 is to design the workflow first and select tools second. Start with custody. Define invoice states. Make webhooks reliable. Build reconciliation early. Give support a real view. Then expand supported assets and networks.

The teams that struggle usually did the opposite. They added a button, announced crypto payments, and discovered later that payment state, settlement, refunds, and customer support were the real system.

A crypto merchant account is worth doing when it is treated as infrastructure. That changes the conversation from whether crypto is cool to whether your payment workflow can be trusted in production.

Try coinpayportal.com

You are writing for developers and merchants building crypto payment infrastructure. Try coinpayportal.com.

Try CoinPay

Non-custodial crypto payments — multi-chain, Lightning-ready, and fast to integrate.

Get started →