Blockchain Merchant Account Architecture: A Practical 2026 Guide for Developers and Merchants

Most teams start looking for a blockchain merchant account when checkout becomes the obvious bottleneck. They want a place to accept crypto, generate invoices, and mark orders as paid. That sounds simple until the first customer sends the wrong amount, pays after expiry, uses the wrong chain, or opens a support ticket with only a transaction hash.

Teams think the problem is account approval. The real problem is payment state.

A blockchain merchant account is not just a hosted dashboard or a crypto address generator. In production, it becomes the operating layer between your store, your wallet policy, your accounting system, your support team, and the blockchains you accept. That changes the conversation.

The practical question is not which provider has the nicest checkout page. The practical question is whether your payment architecture can survive retries, chain delays, underpayments, refunds, disputes, wallet rotation, webhook failures, and month-end reconciliation without turning every payment into a manual investigation.

Table of contents

- Why a blockchain merchant account is an operating system, not a signup form

- Blockchain merchant account architecture in 2026

- Merchant onboarding and account model

- Payment flow from invoice to finality

- Webhooks, idempotency, and reconciliation

- Custody, escrow, and dispute handling

- Fees, pricing, and settlement operations

- Security, compliance, and risk controls

- What breaks when implementation is poor

- Build or buy: choosing blockchain merchant account infrastructure

- Product fit: where coinpayportal.com belongs

Why a blockchain merchant account is an operating system, not a signup form

The merchant account now owns state

In card payments, many merchants are trained to think in terms of authorization, capture, settlement, and chargebacks. Crypto payments look simpler because there is no card network authorization step. That simplicity is misleading.

A crypto payment has a different set of states:

- Invoice created

- Address or payment request assigned

- Transaction detected

- Transaction seen but not confirmed

- Transaction confirmed below threshold

- Transaction confirmed enough to release order

- Payment underpaid or overpaid

- Payment expired but later received

- Refund requested

- Settlement recorded

The mistake teams make is treating blockchain detection as the same thing as order completion. A mempool event is not finality. One confirmation is not always enough. A transaction hash is not an accounting entry. A wallet balance is not a ledger.

Practical rule: never let a raw blockchain event update an order directly. Route it through a payment state machine with idempotency, confirmation policy, and reconciliation.

A useful way to think about it is this: the blockchain is the settlement rail, not your application ledger. Your merchant account has to translate unpredictable public-chain behavior into predictable business events.

The UI is the smallest part

A checkout button is easy. The hard parts appear after the button:

- Which asset was quoted?

- Which chain was used?

- Was the amount exact after fees?

- Did the customer pay from an exchange wallet that batched transactions?

- Did the payment arrive after the invoice expired?

- Who can issue refunds?

- Where does the merchant see settlement status?

- What happens if the webhook endpoint is down?

This is why a blockchain merchant account should be evaluated as infrastructure, not as a payment widget. The checkout page is just one interface into a larger workflow.

If you are still at the setup stage, the adjacent architecture decisions are covered in more depth in our guide to crypto payment gateway setup, especially around custody boundaries and webhook state.

Blockchain merchant account architecture in 2026

Core components

A production blockchain merchant account usually needs five layers:

- Checkout and invoice creation

- Address or payment request management

- Blockchain monitoring and confirmation tracking

- Merchant ledger and reconciliation

- Settlement, refund, and support workflows

The provider may hide some of this behind an API, but the functions still exist. If nobody owns one of these layers, the gap usually shows up as a support problem later.

A practical architecture looks like this:

| Layer | What it does | What breaks if ignored |

|---|---|---|

| Invoice service | Creates amount, asset, chain, expiry, metadata | Orders cannot map reliably to payments |

| Address management | Assigns payment addresses or requests | Reused addresses create privacy and reconciliation issues |

| Chain monitor | Watches transactions and confirmations | Payments are missed or marked paid too early |

| State machine | Converts events into merchant-facing status | Duplicate webhooks corrupt order state |

| Ledger | Records expected, received, settled, refunded | Finance cannot close books |

| Support tools | Lets staff search by order, wallet, hash, customer | Every exception becomes an engineering ticket |

The architecture does not need to be complicated. It needs to be explicit.

Custody and settlement boundaries

Custody is the line that determines who can move funds. Settlement is the process that determines when funds become available to the merchant. They are related, but not the same.

A non-custodial account may help the merchant accept payments without taking possession of funds. A custodial account may hold balances and later pay out. An escrow flow may hold funds until a condition is satisfied. Each model changes the risk surface, the operational workflow, and the user experience.

The practical question is: where can money sit, who can move it, and what evidence proves that movement happened?

Teams in decentralized compute and payment-adjacent infrastructure face similar boundary problems when work, validation, and settlement are split across systems. Related reading from our network: IBM Quantum Computing in 2026: A Practical Architecture for Decentralized Compute Builders.

Merchant onboarding and account model

Business identity, wallets, and roles

A blockchain merchant account should model the merchant as more than an email address. In production, you need separate concepts for:

- Business profile

- Store or application

- API keys

- Wallets and payout destinations

- Staff roles

- Settlement preferences

- Risk settings

- Webhook endpoints

This matters because the person integrating the API is often not the person managing refunds or settlement. Developers need keys and logs. Finance needs exports. Support needs transaction search. Owners need payout controls.

A weak account model usually starts with one admin login and one wallet address. It works for the first test payment. It fails when the merchant hires support staff, adds another store, changes wallets, or needs to audit who changed a payout address.

Practical rule: separate developer access, operational access, and money movement permissions. If one role can do everything, your account model is not ready for real merchant operations.

Network and asset policy

Accepting crypto payments does not mean accepting every token on every chain. That is how teams create support debt.

A merchant account should define:

- Supported networks

- Supported assets per network

- Minimum and maximum payment amounts

- Confirmation thresholds

- Expiry windows

- Overpayment and underpayment policy

- Refundable assets

- Payout destinations

For example, accepting USDC on multiple chains sounds merchant-friendly. In practice, it requires clear chain selection, address handling, network warnings, and support tooling. A customer sending USDC on the wrong network may create an expensive recovery case or an unrecoverable loss.

The mistake teams make is adding assets before they have support workflows. Asset coverage is not a feature if every edge case needs a founder in Telegram.

Payment flow from invoice to finality

State machine you actually need

The payment flow should be deterministic even when the chain is not. Here is a practical sequence:

- Customer starts checkout and selects crypto payment.

- Merchant backend creates an order in pending payment state.

- Merchant account creates an invoice with amount, asset, chain, expiry, and order metadata.

- Customer receives an address, QR code, or payment request.

- Chain monitor detects an incoming transaction.

- Payment enters detected state, not paid state.

- Confirmation policy runs based on asset, chain, amount, and risk.

- Payment moves to confirmed or exception state.

- Merchant order updates through an idempotent callback or polling result.

- Ledger records received amount, expected amount, fees, and settlement status.

This is the difference between a demo and production. In a demo, a detected transaction is enough. In production, detected is only one state in the workflow.

A compact state model might look like:

created -> awaiting_payment -> detected -> confirming -> paid

| |

| -> failed_risk_check

-> underpaid

-> overpaid

-> expired_late_payment

paid -> settled

paid -> refund_pending -> refunded

Do not overload paid to mean detected, confirmed, credited, and settled. Those are different events with different business consequences.

Confirmations, expiry, and underpayments

Confirmation policy should be configurable. Low-value payments on fast networks may need a different rule than high-value payments on slower chains. Stablecoin payments may have different operational risk than native asset payments. The point is not to invent complexity. The point is to avoid hardcoded assumptions.

Invoice expiry also needs careful handling. If a customer pays after expiry, you still have funds on-chain. Your system needs to decide whether to credit, refund, or hold for review.

Underpayments are even more common. They happen because of exchange withdrawal fees, wallet fee settings, user error, or price movement when quotes are not locked. Your merchant account should support a policy such as:

- Accept small underpayments within a tolerance

- Request top-up for meaningful underpayments

- Hold for manual review above a threshold

- Refund when fulfillment cannot proceed

Practical rule: every invoice needs an exception path. If the only happy path is exact payment before expiry, your support team will become the payment processor.

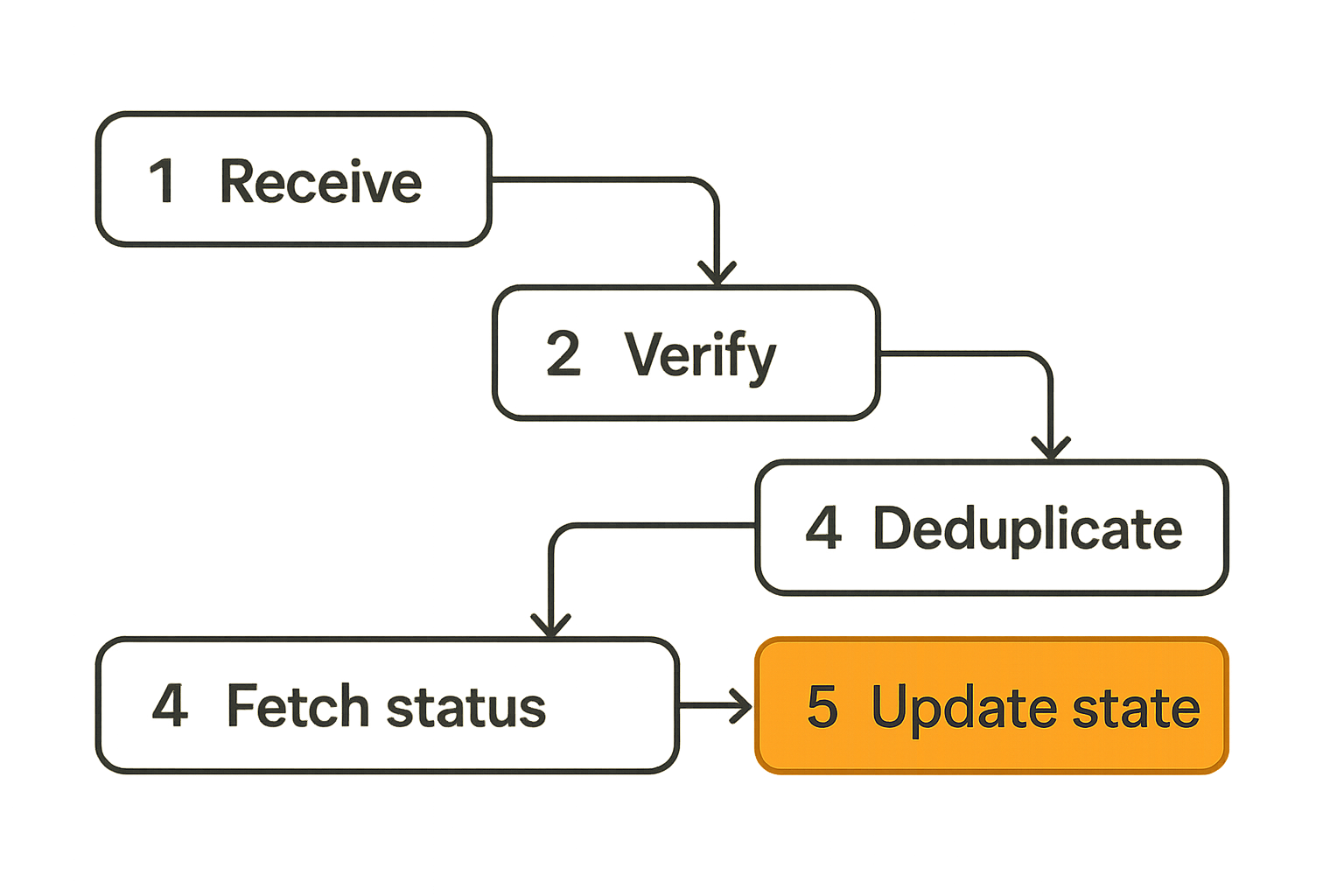

Webhooks, idempotency, and reconciliation

Webhooks are signals, not truth

Webhooks are delivery mechanisms. They are not the source of truth. This distinction prevents a lot of production damage.

Your application should assume webhooks can be delayed, duplicated, reordered, or missed. That means every webhook handler needs:

- Signature verification

- Idempotency by event ID and payment ID

- Safe retries

- Status fetching from the provider API

- No direct irreversible fulfillment on untrusted payloads

- Durable logging

The mistake teams make is writing a webhook handler that says: if status equals paid, ship the order. That may work until duplicate events, replay attempts, or state regressions appear.

A safer pattern:

receive webhook

verify signature

store event if new

fetch payment status from API

compare status transition against local state machine

update order only if transition is valid

acknowledge webhook

If your team wants API-level references while integrating, keep the provider developer documentation beside your implementation checklist rather than relying only on dashboard testing.

Ledger reconciliation loop

Reconciliation is where crypto payment systems either become reliable or become folklore. You need to match at least four records:

- Merchant order

- Payment invoice

- On-chain transaction

- Ledger entry

For each payment, your system should be able to answer:

- What did we expect?

- What did we receive?

- What did we credit to the order?

- What fees were applied?

- What was settled to the merchant?

- Was anything refunded?

A daily reconciliation job should compare provider records, internal orders, and chain-level references. It should not depend on someone noticing a mismatch in the dashboard.

One useful implementation sequence:

- Pull all payments updated since the last reconciliation run.

- Compare each payment with local order state.

- Flag paid payments without fulfilled orders.

- Flag fulfilled orders without confirmed payment.

- Match transaction hashes against ledger records.

- Export settlement and fee records for finance.

- Create support tasks for unresolved exceptions.

This loop is boring. That is the point. Boring payment operations are usually healthy payment operations.

Custody, escrow, and dispute handling

Non-custodial versus custodial paths

A blockchain merchant account can be custodial, non-custodial, or a hybrid. The right model depends on the business.

| Model | Funds controlled by | Best fit | Operational tradeoff |

|---|---|---|---|

| Non-custodial | Merchant wallet or merchant-controlled destination | Merchants that want direct control | Merchant must own wallet security and accounting |

| Custodial | Provider until payout | Merchants that want simplified balances | Provider risk and payout dependency increase |

| Escrow | Contract, provider, or agreed workflow until release | Marketplaces, services, high-trust transactions | More states, more disputes, more support logic |

Non-custodial does not mean no operations. It means the merchant must understand wallet security, settlement records, refunds, and tax reporting. Custodial does not mean bad. It means you need stronger review of payout terms, account controls, and failure scenarios.

The practical question is not whether custody is good or bad. The practical question is whether the custody model matches the merchant workflow.

When escrow changes the workflow

Escrow is useful when payment and fulfillment are separated by trust. Marketplaces, service businesses, digital deliverables, and high-value transactions often need a release step instead of immediate settlement.

Escrow changes the account model because funds may pass through additional states:

- Funded

- Awaiting delivery

- Buyer review

- Dispute opened

- Released to seller

- Refunded to buyer

- Split settlement

That means support tooling matters. You need a way to show both sides what happened, when funds were received, what conditions apply, and who can release or dispute. If your business needs conditional release rather than simple checkout, evaluate a dedicated crypto escrow workflow early instead of bolting it on after disputes begin.

Privacy tools and encrypted collaboration systems face a similar issue: the hard part is not only encryption, but trust, identity, device state, and recovery. Related reading from our network: End to End Encryption Messaging in 2026: A Practical Architecture for Private Teams.

Fees, pricing, and settlement operations

Network fees and merchant fees

Crypto fees are not one number. A merchant account may involve:

- Network transaction fees

- Provider processing fees

- Conversion spreads

- Refund transaction fees

- Withdrawal or payout fees

- Minimum settlement thresholds

Merchants care about net settlement, not just advertised processing fees. Developers need the fee model exposed clearly enough to display accurate order totals and reconcile accounting entries.

The mistake teams make is hiding fees until settlement. That creates finance friction and support tickets. If a merchant sees a payment for 100 units and settlement for 98.70 units, the system should explain the difference without a spreadsheet archaeology project.

A useful ledger entry should separate:

- Gross amount expected

- Gross amount received

- Network fee, if relevant

- Provider fee

- FX or conversion difference

- Net amount settled

- Settlement transaction reference

FX, stablecoins, and payout timing

Stablecoins reduce volatility, but they do not remove settlement operations. You still have network selection, token contract risk, liquidity, payout timing, and chain congestion.

For merchants pricing in fiat, you need a quote policy:

- Lock the rate for a defined window

- Requote after expiry

- Decide who absorbs price movement

- Store the rate used at invoice creation

- Store the rate used at settlement, if conversion occurs

For merchants pricing directly in crypto, you still need clear reporting in the merchant's accounting currency.

Payout timing should also be explicit. Some merchants want immediate forwarding to a wallet. Others want daily or weekly settlement. Some want stablecoin balance management. Each choice affects reconciliation and support.

Practical rule: do not treat settlement as a background detail. Settlement timing, fees, and references should be first-class merchant account data.

Security, compliance, and risk controls

Key management and permissions

API keys are money-adjacent credentials. Treat them accordingly.

A blockchain merchant account should support separate keys or scopes for actions such as:

- Creating invoices

- Reading payment status

- Managing webhooks

- Issuing refunds

- Changing payout wallets

- Exporting reports

At minimum, production and test keys should be separate. Keys should be rotatable without downtime. Webhook secrets should not be reused across stores. Sensitive account changes should produce audit logs.

For merchant applications, avoid putting secret keys in front-end code. The browser should never create privileged payment instructions directly. Use your backend to create invoices, attach order metadata, and validate state transitions.

A basic backend flow:

client requests checkout

server validates cart and customer session

server creates local pending order

server creates crypto invoice using secret key

server returns hosted checkout URL or payment details

client displays payment instructions

server waits for verified status update

Screening without blocking the business

Risk controls should reduce bad payments without turning every legitimate customer into a manual review case. Depending on the merchant, controls may include transaction screening, limits, velocity checks, geofencing, sanctions policy, or manual review for high-value payments.

The key is to connect risk decisions to payment state. If a payment is detected but fails a risk rule, the order should not silently remain pending forever. It should move to a review state with clear internal action.

What breaks in practice is disconnected tooling. The risk dashboard says review. The order system says pending. The support agent sees neither. The customer sees paid. That gap creates the worst kind of payment incident: one where every system is partially correct.

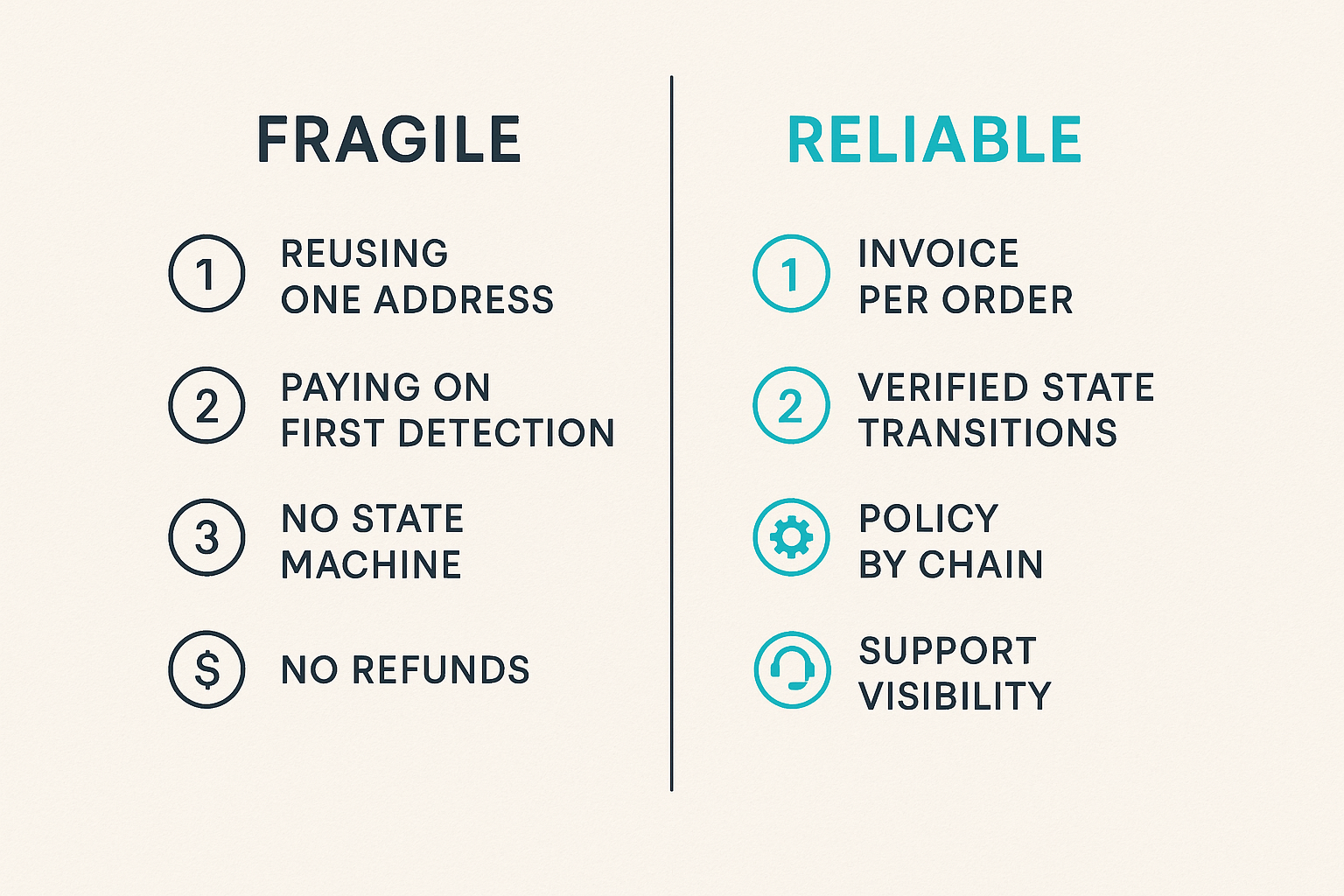

What breaks when implementation is poor

Common failure modes

Most blockchain merchant account failures are not caused by exotic chain events. They are caused by ordinary workflow gaps.

Common problems include:

- Reusing one address for all orders

- Marking orders paid on first detection

- No idempotency in webhook handlers

- No local payment state machine

- No way to handle late payments

- No underpayment policy

- No refund workflow

- No audit trail for payout wallet changes

- No reconciliation job

- No support search by transaction hash

The operational symptom is always similar: engineers become the escalation path for routine payment questions. A customer sends a hash, support cannot find the order, finance cannot match settlement, and the founder asks someone to inspect the chain manually.

That is not a blockchain problem. That is a workflow design problem.

What works and what fails

| Area | What fails | What works |

|---|---|---|

| Checkout | Static address pasted into UI | Invoice per order with metadata |

| Webhooks | Direct order mutation from payload | Verified, idempotent state transitions |

| Confirmations | One hardcoded rule for every payment | Policy by chain, asset, amount, and risk |

| Reconciliation | Manual dashboard checks | Scheduled ledger comparison and exception queue |

| Refunds | Ad hoc wallet sends | Refund records tied to original payment |

| Support | Search only by order ID | Search by order, invoice, wallet, hash, customer |

| Settlement | Balance viewed as accounting | Ledger entries with fees and payout references |

The pattern is straightforward. Systems fail when payment data is treated as a notification. Systems work when payment data is treated as a ledgered workflow.

Streaming and subscription businesses see similar state problems even outside payments: access, entitlement, device state, billing, and support have to agree. Related reading from our network: Fubo Streaming in 2026: A Practical Architecture for Cord Cutters, IPTV Viewers, and Home Media Setups.

Build or buy: choosing blockchain merchant account infrastructure

When to build

Build your own infrastructure when the payment flow is core to your product and you have the operational capacity to own it. Examples include wallets, exchanges, protocol-native marketplaces, high-volume fintech platforms, and businesses with custom settlement logic.

If you build, budget for more than API calls. You need chain indexing or reliable providers, address management, monitoring, confirmations, fee tracking, refund tooling, reporting, and support interfaces. You also need engineering coverage when something breaks outside office hours.

Building can make sense when:

- You need custom custody logic

- You operate at enough scale to justify dedicated payment engineering

- You need deep integration with proprietary ledger systems

- You have compliance, risk, or reporting requirements that off-the-shelf systems cannot satisfy

- You can maintain chain-specific behavior over time

The mistake teams make is comparing build cost against the first checkout demo. Compare it against the full production lifecycle.

When to use a gateway

Use a gateway or merchant account provider when your business needs reliable crypto acceptance but does not need to own every rail internally. Most merchants, SaaS products, agencies, digital sellers, and early marketplaces fit here.

A gateway is especially useful when you want:

- Faster launch

- Hosted checkout or simple API integration

- Webhook-based order updates

- Merchant dashboards

- Escrow or dispute workflows

- Refund and settlement tooling

- Documentation your team can implement against

This does not remove architecture responsibility. You still need local order state, idempotent handlers, reconciliation, and support workflows. But it lets your team focus on your business rather than maintaining payment rail plumbing.

If you are choosing between direct integration options and a provider, our broader guide on how to accept crypto payments covers the merchant-side decision points without assuming every business needs the same setup.

Product fit: where coinpayportal.com belongs

Architecture fit for developers and merchants

coinpayportal.com fits teams that want a practical blockchain merchant account workflow without turning crypto payments into a permanent infrastructure project.

For developers, the important pieces are predictable integration surfaces: invoice creation, payment status, webhooks, documentation, and enough state clarity to keep your order system honest. For merchants, the important pieces are operational: real-time processing, fee handling, settlement visibility, and workflows that support actual customer issues rather than pretending they will not happen.

The right product fit is not about hype. It is about reducing the number of payment cases that require manual chain inspection.

A good implementation with coinpayportal.com should still follow the same rules:

- Create local orders before invoices

- Store provider payment IDs

- Verify webhook signatures

- Treat webhooks as signals

- Fetch payment status before fulfillment

- Reconcile daily

- Keep refund and settlement records tied to original payments

That is the architecture that makes a blockchain merchant account useful in 2026: not just payment acceptance, but operational clarity from checkout through settlement.

Try coinpayportal.com

You are writing for developers and merchants building crypto payment infrastructure. If you need a blockchain merchant account that respects checkout state, merchant operations, and production workflows, Try coinpayportal.com.

Try CoinPay

Non-custodial crypto payments — multi-chain, Lightning-ready, and fast to integrate.

Get started →