Threat Intelligence Blockchain Architecture for Crypto Payment Teams

A crypto checkout can look healthy while the operation behind it is exposed. The invoice is created, the wallet receives funds, the webhook fires, and the merchant dashboard shows paid. Then someone asks whether the sender wallet is tied to scams, sanctions exposure, stolen funds, mixer activity, or a customer support case from last week.

That is when threat intelligence blockchain stops being a research topic and becomes a payment architecture problem.

Teams think the problem is finding a tool that can label wallets. The real problem is deciding where risk signals enter the payment lifecycle, who owns the decision, how long funds can sit in review, and how the business reconciles that state later.

The practical question is not whether blockchain intelligence is useful. It is how to make it operational without breaking checkout conversion, support workflows, settlement, or developer sanity.

This guest contribution is written from the security operations side by the team at threatcrush.com, but the focus here is merchant infrastructure: APIs, webhooks, state machines, reconciliation, and the boring details that determine whether a crypto payment system survives production traffic.

Table of contents

- Why threat intelligence blockchain belongs in payment architecture

- What blockchain threat intelligence changes in production

- The minimum signal model for crypto merchants

- Workflow from invoice creation to settlement

- Decision policies approve, hold, reject, escalate

- What breaks when teams bolt intelligence on later

- Data architecture for auditability and reconciliation

- Developer patterns that keep the integration sane

- Metrics that matter for threat intelligence blockchain operations

- Product fit where CoinPayPortal sits in the stack

- Closing checklist for 2026 deployments

Why threat intelligence blockchain belongs in payment architecture

Threat intelligence blockchain workflows belong close to payment state because the decision affects money movement. If the signal arrives after fulfillment, settlement, or withdrawal, the team is no longer managing risk. It is managing cleanup.

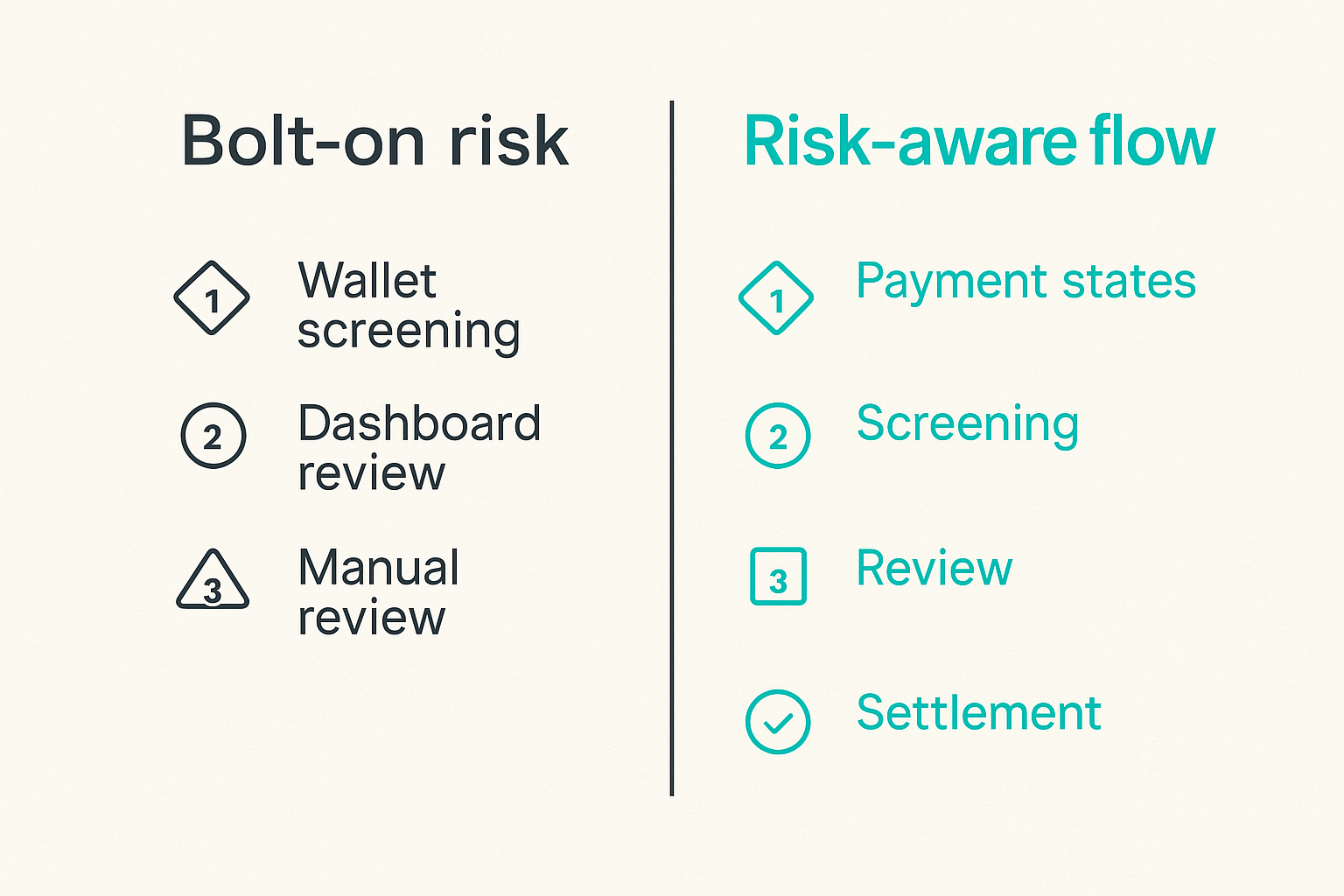

The checkout UI is not the control plane

The mistake teams make is treating crypto risk as a front-end badge. They add a check beside a wallet field, maybe query a provider before showing a deposit address, and call the job done.

That misses the real control point. A crypto payment is not a single UI event. It is a sequence of states: invoice created, address assigned, transaction detected, confirmations observed, amount matched, risk assessed, order fulfilled, funds swept, funds settled, case closed.

Threat intelligence has to bind to those states. If it only exists at checkout time, it will miss the transaction that arrives from a different sender, the underpayment that gets topped up from another wallet, the delayed confirmation after a risk score changes, or the merchant refund that creates secondary exposure.

Risk signals need somewhere to land

A useful way to think about it is this: intelligence is not a verdict until the payment system can act on it. The raw signal might say suspected scam exposure, high-risk exchange, mixer interaction, ransomware cluster, bridge exploit, darknet market adjacency, or low-confidence attribution. The payment platform still has to translate that into an operational state.

That means the architecture needs a place for risk data, a policy layer, an audit trail, and an exception queue. Without those pieces, blockchain intelligence becomes another dashboard nobody checks until after a bad payment has already moved through the business.

Practical rule: Do not buy threat intelligence for crypto payments unless you know which payment states it is allowed to change.

What blockchain threat intelligence changes in production

In production, blockchain threat intelligence changes timing, ownership, and liability boundaries. It does not simply add more data. It forces the merchant to decide what happens when a payment is technically valid but commercially risky.

From address lookup to decision engine

Address lookup is a starting point. It answers one narrow question: what is known about this address right now? A payment decision engine answers a better question: given this customer, invoice, chain, amount, asset, merchant policy, and current intelligence, what should happen next?

That changes the conversation. The output is not just risk score equals 82. The output is hold fulfillment, request review, accept but delay settlement, reject and refund manually, or escalate to compliance. For developers, this is the difference between an API response and a workflow.

| Approach | What it does | What breaks in practice |

|---|---|---|

| One-time wallet screening | Checks a supplied address before payment | Sender may differ from the entered wallet |

| Post-payment dashboard review | Lets operators inspect payments later | Fulfillment may already be complete |

| Risk-aware payment state | Screens transaction context before action | Requires policy design and state handling |

| Manual-only review | Sends suspicious payments to humans | Does not scale without triage and queues |

Where the signal enters the payment lifecycle

There are three common insertion points.

First, pre-payment screening checks a customer-provided refund or sender address. This is useful, but incomplete. Second, transaction-time screening checks the actual on-chain transaction, inputs, outputs, asset, chain, and counterparty data. This is where most useful payment decisions happen. Third, post-settlement monitoring catches retroactive intelligence updates and downstream exposure.

Most merchants need all three, but not at the same sensitivity. A high-risk signal before fulfillment may block the order. The same signal discovered weeks later may create a review task, not an automatic reversal.

The minimum signal model for crypto merchants

A merchant does not need every graph feature a blockchain analytics vendor can produce. It needs a signal model that maps to decisions. Over-collecting creates noise. Under-collecting creates blind spots.

Address, transaction, cluster, and behavioral signals

At minimum, store four categories.

- Address signals: labels, category, ownership hints, direct exposure, watchlist status.

- Transaction signals: hash, chain, asset, amount, confirmation count, source and destination context.

- Cluster signals: entity-level relationships where a provider groups addresses together.

- Behavioral signals: payment timing, repeated underpayments, rapid address reuse, velocity, mismatched customer metadata.

The merchant should not treat these as equal. A direct sanctioned address label is different from weak proximity to a risky cluster. A first-time buyer sending exact amount from a reputable exchange is different from ten invoices paid from rotating wallets with inconsistent amounts.

Confidence, freshness, and source separation

Threat intelligence decays. Labels change. Clusters split. Providers disagree. If your system stores only a final risk score, you cannot explain why a payment was held or why the same wallet was accepted last month.

Store confidence, timestamp, provider, version, and reason codes. Keep source data separate from merchant policy. The provider can say high mixer exposure. The merchant policy decides whether that means hold, reject, or review.

A simple internal model can look like this:

risk_event:

payment_id: pay_7391

chain: bitcoin

tx_hash: tx_abc

provider: screening_vendor_a

provider_score: 74

confidence: medium

reasons:

- mixer_exposure

- high_velocity_source

observed_at: 2026-05-25T10:18:00Z

policy_action: manual_reviewPractical rule: Store the reason and context behind every risk decision. A score without a reason is not audit data; it is a support problem waiting to happen.

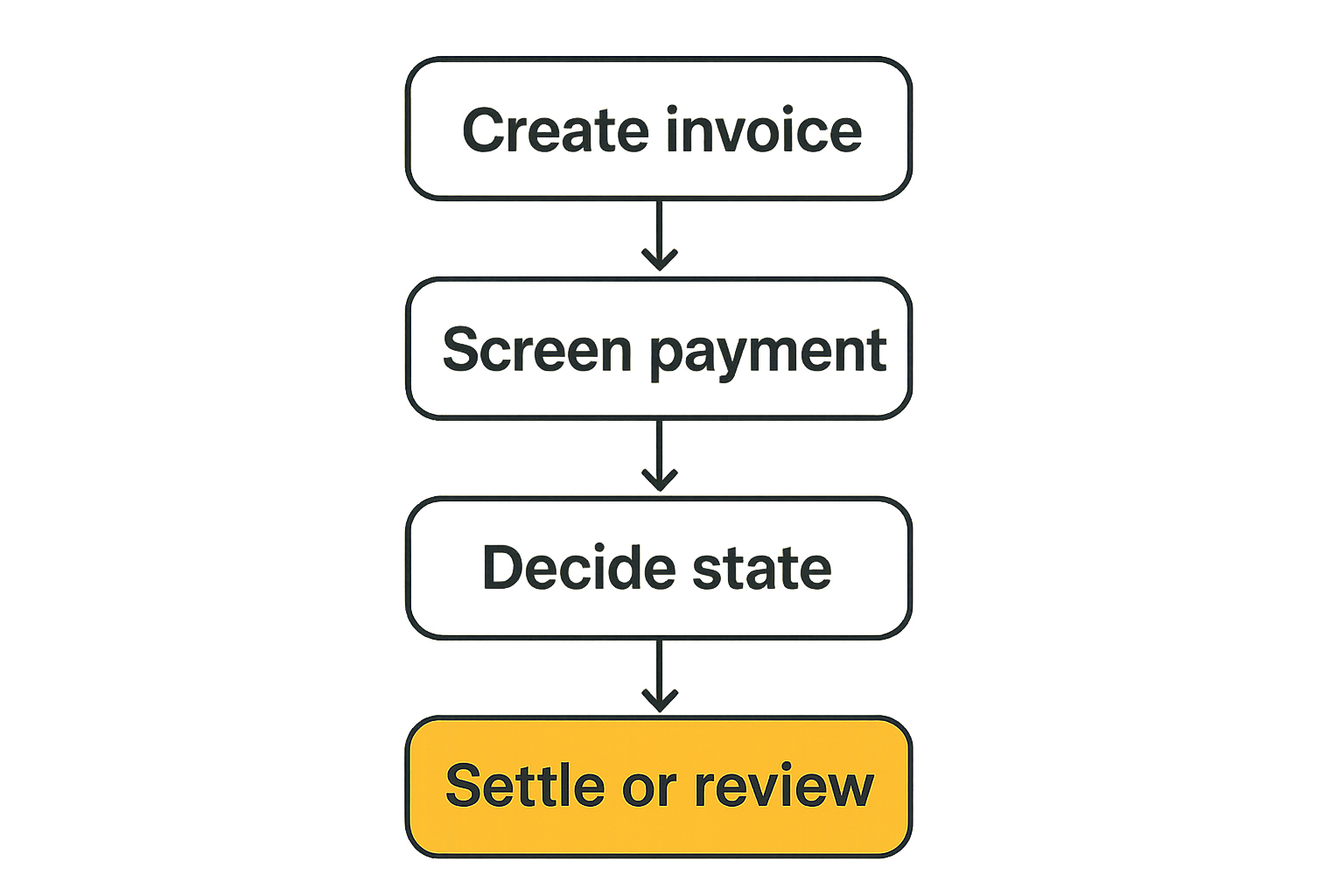

Workflow from invoice creation to settlement

The practical question is how to wire intelligence into the payment workflow without turning checkout into a slow compliance ceremony. The answer is not one giant synchronous call. It is a state machine with clear fallbacks.

A practical implementation sequence

A production-ready sequence usually looks like this:

- Create invoice with chain, asset, amount, expiration, merchant account, customer reference, and fulfillment rules.

- Assign payment address or payment request, then optionally screen any customer-provided wallet metadata.

- Detect on-chain transaction and match it to invoice amount, asset, chain, and confirmation policy.

- Screen the actual transaction and relevant counterparties using blockchain intelligence.

- Apply merchant policy to create a risk decision: approve, hold, reject, or escalate.

- Emit a payment webhook with both payment state and risk state.

- Fulfill only when the payment state and risk state both satisfy merchant rules.

- Sweep, settle, refund, or hold funds according to operational policy.

- Persist all state transitions for reconciliation and investigation.

That sequence keeps the checkout fast while moving serious decisions to the point where the actual transaction is visible.

Webhooks, retries, and idempotency

What breaks in practice is usually not the intelligence provider. It is webhook handling.

If a merchant receives payment_confirmed before risk_review_completed, the order system may ship early. If the same webhook is retried and processed twice, the merchant may release a held order twice or create duplicate review tasks. If risk data arrives after a timeout, the payment can sit in limbo.

Use separate states, not one overloaded status field:

- payment_state: pending, detected, confirmed, expired, settled, refunded.

- risk_state: not_screened, screening, approved, held, rejected, escalated.

- fulfillment_state: not_ready, ready, fulfilled, blocked, canceled.

Idempotency keys should include payment ID, event type, state version, and provider event ID where available. The handler should be safe to replay.

Practical rule: Never let a single paid flag drive fulfillment for crypto orders. Fulfillment should require both payment validity and risk clearance.

Decision policies approve, hold, reject, escalate

Threat intelligence becomes useful when policy converts messy signals into repeatable actions. The merchant does not need a perfect answer for every signal. It needs a predictable way to handle uncertainty.

Map risk to merchant actions

A clean policy table is better than scattered if statements across services.

| Risk condition | Default action | Operator note |

|---|---|---|

| Direct match to prohibited wallet list | Reject or escalate | Do not auto-refund without policy review |

| High-confidence stolen funds exposure | Hold | Require manual investigation before fulfillment |

| Mixer exposure above threshold | Review | Sensitivity depends on merchant category |

| Low-confidence adverse label | Approve with logging | Monitor for repeat behavior |

| Provider timeout | Temporary hold or degraded approval | Depends on order value and merchant risk tolerance |

The important part is consistency. Operators should be able to answer why two payments received different treatment. Developers should be able to change thresholds without redeploying the checkout service.

Keep policy separate from provider data

Provider data is external intelligence. Policy is a business decision. Mixing them creates lock-in and confusion.

A better design is:

- screening service normalizes provider responses;

- policy service evaluates merchant-specific rules;

- payment service owns payment state;

- order service consumes approved fulfillment events;

- review console handles exceptions.

This separation also helps when a merchant uses multiple providers or changes vendors. The internal policy vocabulary stays stable even if provider reason codes change.

What breaks when teams bolt intelligence on later

Bolting threat intelligence onto an existing crypto checkout usually exposes assumptions that were never written down. The system thought paid meant done. The business thought funds received meant safe. Support thought risk review was someone else's queue.

False positives become support tickets

False positives are not just security noise. In payments, they are customer-facing events. A legitimate customer may pay, see confirmations, and still not receive the product because a risk rule held the order. If the support team cannot see the reason, the customer gets vague answers and the merchant loses trust.

The mistake teams make is hiding risk context in a separate compliance dashboard. Support needs a safe summary: payment held for risk review, reason category, expected review SLA, refund policy, and escalation path. They do not need raw graph analysis, but they do need enough context to avoid making promises the payment team cannot honor.

Investigations lose context

Investigations fail when every system has a fragment. The payment gateway has the transaction hash. The order system has the customer email. The screening provider has the wallet label. The support tool has the complaint. The finance team has the settlement batch.

If those records do not share stable IDs, review becomes archaeology. Operators copy transaction hashes between tools, screenshots replace evidence, and the final decision is hard to defend.

Use a merchant payment ID as the spine. Every event, webhook, risk decision, customer action, and settlement record should point back to it.

Data architecture for auditability and reconciliation

Risk decisions affect financial records. That means the data model has to support auditability, not just real-time decisioning.

Store snapshots, not just verdicts

A verdict is not enough. Approved tells you what happened, but not why. Store the risk snapshot used at decision time, including provider response version, reason codes, timestamps, and policy version.

This matters because blockchain intelligence changes. A wallet accepted today may be labeled next month. That does not necessarily mean the original decision was wrong. It means the system needs to show what was known at the time.

A practical event record includes:

- payment ID and merchant ID;

- chain, asset, amount, transaction hash;

- risk provider and response timestamp;

- normalized reason codes;

- policy version and resulting action;

- actor for manual overrides;

- link to review case if escalated.

Reconcile payment state with risk state

Finance teams reconcile balances. Risk teams reconcile decisions. Crypto payment operations need both.

A payment can be confirmed but held. It can be overpaid and approved. It can be underpaid and rejected for business reasons but still have funds that require manual handling. It can be approved, fulfilled, and later flagged by retroactive intelligence.

Build reconciliation reports that show mismatches:

- confirmed payments with risk_state not approved;

- approved payments not fulfilled after SLA;

- held funds older than policy threshold;

- refunds requested but not executed;

- settled funds tied to later high-risk updates.

This is where the UI is not the system. The system is the ledger of state transitions and decisions.

Developer patterns that keep the integration sane

Payment developers already deal with confirmations, reorgs, rate limits, and webhooks. Threat intelligence adds another external dependency. Treat it like one.

API boundaries and timeout budgets

Do not let checkout availability depend entirely on a risk API. Decide which calls are synchronous, which are asynchronous, and what happens during degraded mode.

For low-value payments, a merchant may accept temporary degraded approval with logging if screening times out. For high-value orders, the same timeout may create a hold. The policy should be explicit.

Useful timeout pattern:

- synchronous pre-check budget: 300 to 800 ms;

- transaction screening budget: async worker with retry;

- provider outage behavior: hold, degrade, or route to backup;

- manual review SLA: visible to support and merchant operators.

Rate limits also matter. If a promotion drives payment volume, risk screening should not collapse under burst traffic. Queue work, batch where safe, and cache immutable lookups carefully.

Queues, dead letters, and manual review

A risk workflow needs a dead-letter queue because some cases will fail. Provider timeout, malformed transaction data, unsupported chain, duplicate webhook, or policy evaluation error should not disappear.

The operational path should be boring:

- failed screening job goes to retry queue;

- repeated failure goes to dead letter;

- dead letter creates an operator task;

- operator decision writes a manual override event;

- payment and fulfillment states update through the same event path as automated decisions.

Manual review should not be a side channel. If an operator approves a payment in a spreadsheet and support fulfills the order manually, the system of record is already broken.

Practical rule: Manual review must write back into the payment state machine. If it does not, reconciliation will fail later.

Metrics that matter for threat intelligence blockchain operations

Threat intelligence blockchain programs should be measured like operations, not like dashboards. More alerts is not success. Better payment decisions with less friction is success.

Measure decision latency and review load

Track how long it takes to move from transaction detected to risk decision. Break it down by chain, asset, merchant, provider, and policy path. A one-minute delay may be fine for a high-value B2B invoice. It may be unacceptable for a low-value digital product checkout.

Review load matters too. If a policy sends 20 percent of payments to manual review, the team will either build a real review process or quietly bypass the policy. Neither outcome should be accidental.

Useful metrics include:

- median and p95 risk decision latency;

- percentage of payments approved automatically;

- percentage held for manual review;

- provider timeout rate;

- average age of held funds;

- manual override rate by operator and merchant.

Track reversals, disputes, and released funds

Crypto payments are often framed as irreversible, but merchant operations still have reversals in the practical sense: refunds, credits, cancellations, chargeback-like support disputes, and account closures.

Track what happens after a risk decision. How many held payments are eventually released? How many rejected payments become support escalations? How many approved payments later receive adverse labels? How many refunds create new exposure?

This closes the loop. Without outcome tracking, the policy never improves. It only gets stricter or looser based on anecdotes.

Product fit where CoinPayPortal sits in the stack

A payment platform cannot replace every specialized blockchain intelligence provider. It also should not pretend risk is just a label attached to a wallet. The useful product surface is orchestration: payment state, webhook delivery, merchant settings, settlement awareness, and the places where a risk decision changes what happens next.

Payment orchestration needs risk-aware state

For merchants and developers, the value is having payment state and operational hooks in one place. If CoinPayPortal is creating invoices, listening for transactions, emitting webhooks, and supporting settlement workflows, then it is also the natural place to expose risk-aware states to merchant systems.

That does not require turning the payment gateway into a full intelligence vendor. It requires clean extension points:

- attach screening results to payment events;

- expose risk_state separately from payment_state;

- let merchants configure hold and fulfillment policies;

- support manual review and override events;

- preserve audit records for reconciliation.

That is the architecture that lets a merchant use blockchain intelligence without wiring every order system directly to every risk provider.

When to build versus integrate

Build the state machine. Integrate the intelligence.

Most merchants should not build their own entity clustering, attribution system, or illicit exposure graph. That is specialized work. But merchants do need to own their policy, customer experience, fulfillment rules, and financial records.

A good integration boundary keeps these concerns separate. Intelligence providers supply signals. CoinPayPortal-style payment infrastructure coordinates payment state. The merchant decides business policy.

Closing checklist for 2026 deployments

Threat intelligence blockchain work in 2026 is moving from optional dashboard to payment infrastructure. Regulators, banking partners, enterprise customers, and internal finance teams increasingly expect merchants to know how risky funds are handled. But the best systems will still be the ones that keep checkout reliable and operations clear.

What works

Use this checklist before launching or refactoring a crypto payment risk workflow:

- Define which payment states risk intelligence can change.

- Screen the actual transaction, not only the customer-entered wallet.

- Store provider response, reason codes, timestamps, and policy version.

- Keep payment_state, risk_state, and fulfillment_state separate.

- Make webhook handlers idempotent and replay-safe.

- Give support a safe explanation for held payments.

- Route exceptions into a real review queue.

- Reconcile held, released, refunded, and settled funds.

- Measure decision latency, review load, and outcomes.

What fails

The failure pattern is predictable. Teams add a wallet score API, wire it into checkout, and do not change the rest of the system. Then the first edge case arrives: a transaction from a different wallet, a provider timeout, a false positive, a retroactive label, or a manual refund.

What fails is not the idea of blockchain intelligence. What fails is the assumption that intelligence can live outside the payment workflow.

The practical architecture is risk-aware payment orchestration: signals enter at the right time, policy converts them into actions, state machines prevent premature fulfillment, and reconciliation proves what happened later. That is how threat intelligence blockchain becomes useful for merchants instead of becoming another dashboard in the stack.

Try coinpayportal.com

CoinPayPortal helps developers and merchants build crypto checkout flows with payment state, webhooks, and settlement operations in one place. Try coinpayportal.com

Try CoinPay

Non-custodial crypto payments — multi-chain, Lightning-ready, and fast to integrate.

Get started →