AI Agents Blockchain Payments: Practical Architecture for Merchants and Developers

AI agents blockchain payments sound like a future-looking feature until a merchant asks a simple question: who is allowed to spend, how much, for what, and what happens when the agent is wrong?

Teams think the problem is making an AI agent call a wallet or payment API. The real problem is building a payment workflow where autonomous software can request, authorize, settle, reconcile, and recover from failures without turning merchant operations into a support queue.

That changes the conversation. The practical question is not whether an agent can submit a transaction. It can. The practical question is whether your checkout, wallet policy, webhook processing, and reconciliation stack can safely handle non-human buyers and software-driven merchants.

In 2026, this matters because agents are moving from demos into procurement, support, commerce, developer tooling, and backend automation. If agents can compare vendors, order compute, renew subscriptions, buy digital goods, or trigger payouts, then payments are no longer a final screen. Payments become part of the agent runtime.

Table of contents

- Why ai agents blockchain is a payment architecture problem

- The basic stack for ai agents blockchain payments

- Payment flows that actually work for agents

- Where trust breaks when agents spend crypto

- Design the agent wallet boundary before the checkout

- Implementation workflow for agent-ready crypto payments

- What works and what fails in production

- Metrics merchants should track for ai agents blockchain payments

- Security compliance and support realities

- How CoinPayPortal fits into the agent payment layer

- Closing checklist for ai agents blockchain payments

Why ai agents blockchain is a payment architecture problem

The UI is not the system

The mistake teams make is treating ai agents blockchain payments like a new checkout surface. They imagine an agent clicking a payment button, approving a wallet prompt, or calling a simple pay() function.

That is the smallest part of the system.

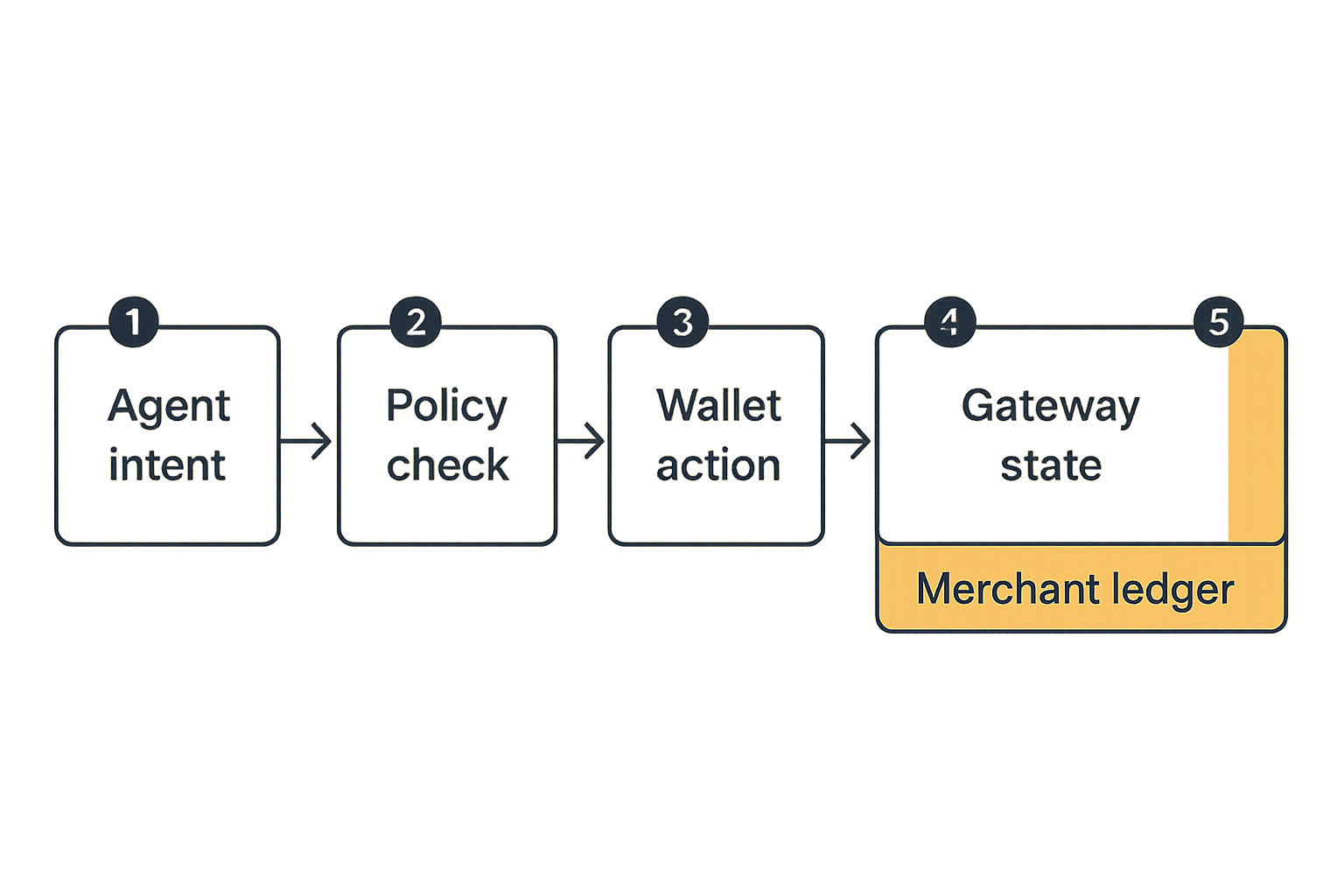

A real crypto payment flow includes quote creation, address generation, network selection, token handling, expiry windows, transaction monitoring, confirmation policy, webhook delivery, merchant order status, settlement records, refunds, and support tooling. If an agent participates in that flow, it does not remove those responsibilities. It adds new ones.

A human buyer can read a warning, notice a wrong amount, call support, or abandon checkout. An agent may keep retrying, submit the wrong asset, pay after expiry, or execute a purchase based on stale context. Your payment stack has to assume the buyer may be software with partial memory and limited judgment.

Practical rule: do not let the agent be the system of record for payment state. The payment platform, merchant backend, and ledger should own state transitions.

A useful way to think about it is this: the agent can initiate intent, but your infrastructure must validate authorization, amount, asset, chain, expiry, settlement status, and fulfillment rules.

Autonomy changes payment risk

Autonomy turns payment UX into payment policy.

If a user tells an agent, “Buy the cheapest API plan that supports 10 million requests,” the agent may need to compare vendors, create an account, select a plan, pay an invoice, and store credentials. Each step has a different risk profile. Paying $5 for a test API key is not the same as committing $5,000 to an annual contract.

For blockchain payments, the risk is sharper because settlement can be irreversible. You cannot depend on card-style chargebacks to clean up bad decisions. Refunds are possible, but they require operational handling and often a separate outbound payment.

This is where agent payments become an architecture problem:

- Who defines the spend policy?

- Where is the policy enforced?

- Which wallet signs the transaction?

- What happens if the agent pays too late?

- Who receives webhook events?

- Which ledger entry proves the order was paid?

- How does support explain what happened?

If those answers live in prompts, you do not have a payment system. You have a demo.

The basic stack for ai agents blockchain payments

Agent identity and permissions

Before an AI agent can pay, it needs an identity your merchant systems can reason about. This does not mean every agent needs a new blockchain identity standard on day one. It means your backend must distinguish between a human user, an agent acting for that user, an internal automation agent, and a third-party agent acting through an integration.

At minimum, model these fields:

| Field | Why it matters |

|---|---|

principal_user_id | The human or business account responsible for the action |

agent_id | The software actor initiating the workflow |

session_id | The bounded task or conversation that produced the payment intent |

policy_id | The spend and approval rules applied to this action |

merchant_order_id | The merchant-side order or invoice being paid |

payment_intent_id | The payment platform object tracking payment state |

This is not bureaucracy. It is what lets you answer the support question: “Why did this payment happen?”

The team at logicsrc.com works on interoperable AI agent systems and integrations, and this is the pattern we see repeatedly: agent identity is only useful when it is connected to permissions, tools, and downstream business records.

If your agent framework can call tools but your payment gateway only sees anonymous requests, you lose the audit trail. If your payment gateway knows the transaction but your agent runtime cannot map it back to a task, you lose operational context.

Wallets policies and custody boundaries

The wallet model is the core design decision. Everything else follows.

There are three common patterns:

| Model | How it works | Good fit | Main risk |

|---|---|---|---|

| User-controlled wallet | User signs each payment or delegates limited permissions | Consumer purchases, high-trust user actions | Poor automation if every payment needs manual approval |

| Hosted balance | User or business funds an account balance used by the agent | SaaS credits, API usage, recurring tasks | Custody, balance management, and refund complexity |

| Policy-controlled agent wallet | Agent can spend from a wallet under explicit limits | B2B automation, procurement, marketplace agents | Policy bugs can cause real losses |

The practical question is not “Which wallet is most decentralized?” It is “Which wallet boundary matches the merchant’s operating model and risk tolerance?”

For many merchant use cases, a hosted balance or policy-controlled wallet is more realistic than asking a human to sign every action. But those models require clear limits: per transaction, per day, per merchant, per asset, per chain, and per task.

Practical rule: every agent wallet should have a maximum loss boundary. If the agent or integration fails, the blast radius must be known before production.

Payment flows that actually work for agents

Pay per action

Pay-per-action is the simplest agent payment pattern. The agent requests a quote, receives a payment instruction, pays, and waits for confirmation before continuing.

Example use cases:

- Buying a one-time dataset

- Paying for an API key

- Purchasing a digital file

- Triggering a single on-chain service

- Paying a small invoice for a completed task

The payment object should be explicit:

{

"payment_intent_id": "pi_9f31",

"merchant_order_id": "ord_2048",

"amount": "25.00",

"currency": "USDC",

"network": "polygon",

"expires_at": "2026-06-08T15:30:00Z",

"allowed_payers": ["agent_742", "user_118"],

"metadata": {

"task_id": "task_vendor_search_77",

"policy_id": "policy_api_tools_low_risk"

}

}

The agent should not infer payment terms from page text or chat output. It should receive a structured payment instruction from a trusted API. The merchant backend should reject payments that do not match amount, asset, network, order, and expiry rules.

What breaks in practice is stale state. The agent gets a quote, spends time doing other work, then pays after the quote expires or after the order changes. Your backend needs a clean expired state and a way for the agent to request a fresh quote.

Deposits escrow and settlement

For larger or uncertain workflows, pay-per-action gets noisy. Deposits and escrow are better.

A deposit model lets the user fund a balance, then the agent consumes that balance as it performs approved actions. This works well for API usage, compute, support automation, and repetitive merchant tasks.

An escrow model is better when delivery and payment should be separated. For example, an agent hires another agent or service to produce a report. Funds are locked, delivery is verified, and settlement is released when conditions are met.

A basic comparison:

| Flow | Best for | Merchant complexity | Agent complexity |

|---|---|---|---|

| Pay per action | Simple one-time purchases | Low | Low |

| Deposit balance | Repeated small payments | Medium | Medium |

| Escrow | Conditional delivery or marketplaces | High | Medium |

| Subscription | Ongoing access with limits | Medium | Low after setup |

The mistake teams make is forcing every agent payment into a direct transaction. Direct payments are easy to demo and hard to operate at scale. Deposits, balances, and escrow create more backend work, but they reduce transaction friction and improve supportability.

Where trust breaks when agents spend crypto

Prompt intent is not payment intent

A prompt is not a payment authorization.

A user may type, “Find and buy the best plan,” but that sentence is ambiguous. Best by price? Features? Reviews? Contract length? Jurisdiction? Token accepted? Refund policy? An LLM can make a reasonable guess, but payment systems should not settle money based on guesses.

Convert prompt intent into a structured payment intent before any funds move. That conversion should include:

- Merchant identity

- Item or service description

- Amount and currency

- Chain and token

- Expiry

- Refund terms if available

- User or policy authorization

- Agent session reference

The agent may prepare the intent, but your backend should validate it. If the amount exceeds policy, require approval. If the merchant is unknown, require approval. If the asset or network is not allowed, reject it.

Practical rule: treat prompts as untrusted input. Treat payment intents as controlled objects with validation, policy checks, and audit logs.

This is the same principle developers already use for web apps. You do not trust browser form fields just because the UI generated them. Do not trust agent tool calls just because the agent sounded confident.

Webhooks are the source of operational truth

In crypto payments, the frontend is advisory. The chain and payment processor determine truth.

For agent flows, webhooks matter even more because the buyer may not be staring at a confirmation page. The agent may be waiting in a job queue, performing another task, or offline. Your merchant backend needs to react to payment events independently.

A simple webhook handler should do four things:

- Verify the webhook signature.

- Load the payment intent by ID.

- Apply an idempotent state transition.

- Trigger fulfillment only when confirmation policy is satisfied.

Example shape:

async function handlePaymentWebhook(event) {

verifySignature(event);

const payment = await db.paymentIntents.find(event.payment_intent_id);

if (!payment) return ack();

if (alreadyProcessed(event.id)) return ack();

await db.transaction(async (tx) => {

await tx.webhookEvents.insert({ id: event.id, type: event.type });

if (event.type === "payment.confirmed") {

await tx.paymentIntents.update(payment.id, { status: "confirmed" });

await tx.orders.update(payment.merchant_order_id, { status: "paid" });

}

});

return ack();

}

The agent can poll your backend or subscribe to task updates. It should not decide that an order is paid because it broadcasted a transaction. Broadcast is not settlement.

Design the agent wallet boundary before the checkout

Hosted wallet versus user wallet

Most teams start with checkout and postpone wallet design. That is backwards.

The wallet boundary determines security, UX, compliance work, refund handling, and how much autonomy the agent can have. If the user must sign every transaction, the agent is more of an assistant than an autonomous buyer. If the agent controls a funded wallet, the user experience is smooth but the risk controls must be stronger.

Here is the practical tradeoff:

| Question | User wallet | Hosted balance | Policy agent wallet |

|---|---|---|---|

| Can the agent pay unattended? | Rarely | Yes | Yes |

| Who manages private keys? | User | Platform or custodian | Platform, custodian, or smart account |

| Best for high-value payments? | Yes, with approval | Sometimes | Only with strict policy |

| Refund complexity | Medium | Medium to high | High if funds move across accounts |

| Operational burden | Lower custody burden | Higher ledger burden | Higher policy and monitoring burden |

There is no universal winner. A consumer checkout flow may prefer user wallets. A SaaS platform selling usage credits may prefer hosted balances. A procurement agent operating inside a business account may need policy wallets with approval gates.

Spending limits and approval gates

Approval gates are not a sign that the agent is weak. They are how production systems keep autonomy bounded.

Useful controls include:

- Per-transaction maximums

- Daily, weekly, and monthly limits

- Merchant allowlists

- Merchant risk tiers

- Token and network allowlists

- Category restrictions

- Human approval for first-time merchants

- Human approval above thresholds

- Cooldown windows after policy changes

The policy should be evaluated server-side before a payment instruction is issued and again before fulfillment if needed. Do not rely on the agent to remember limits.

A useful policy object might look like this:

{

"policy_id": "policy_ops_agent_01",

"max_single_payment_usd": 100,

"max_daily_usd": 500,

"allowed_assets": ["USDC", "USDT"],

"allowed_networks": ["polygon", "base"],

"approval_required_if": {

"new_merchant": true,

"amount_above_usd": 100,

"subscription_term_months_above": 1

}

}

What breaks in practice is policy drift. A team changes a spending rule in the agent prompt but not in the payment backend. The agent believes it is authorized. The backend disagrees. Or worse, the backend has no policy and accepts the payment.

Implementation workflow for agent-ready crypto payments

Step 1 through step 6

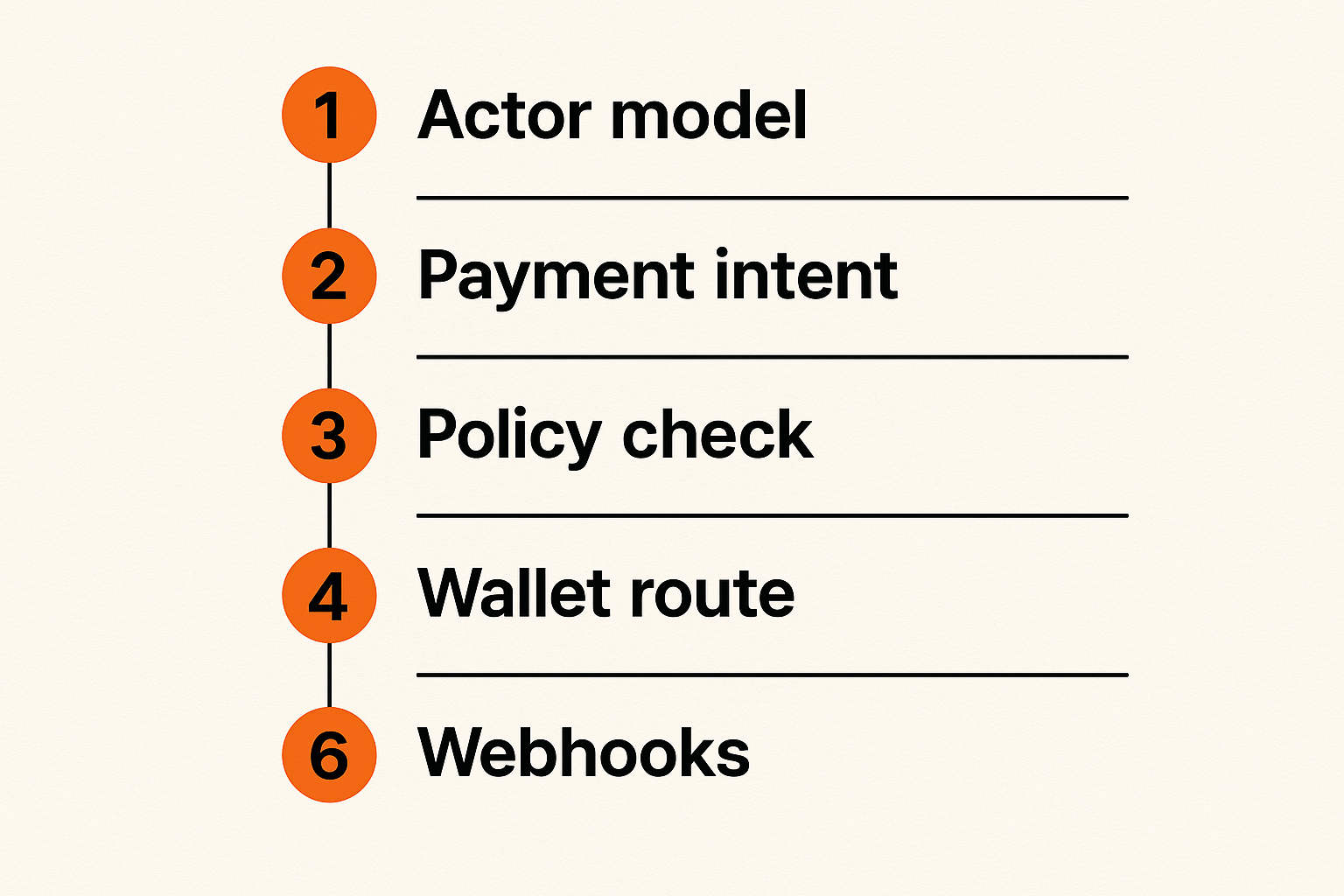

The safest way to build ai agents blockchain payments is to treat the agent as one actor in a normal payment system, not as a replacement for the system.

A practical implementation sequence:

- Define the actor model. Decide how you represent users, businesses, agents, sessions, and policies. Store these IDs on every payment object.

- Create payment intents server-side. The agent can request a payment, but your backend should create the canonical intent with amount, asset, network, expiry, and metadata.

- Evaluate policy before payment instructions. Check spend limits, merchant allowlists, token rules, and approval requirements before returning payment details.

- Route to the correct wallet model. Use user wallet signing, hosted balance debit, or policy wallet execution depending on the account configuration.

- Process webhooks idempotently. Treat blockchain confirmation and processor events as the source of truth for paid, expired, underpaid, overpaid, and failed states.

- Reconcile and expose status. Update merchant orders, agent tasks, customer receipts, and accounting records from the same payment state machine.

This sequence avoids the common trap where the agent creates a transaction and every downstream system tries to interpret it after the fact.

Practical rule: create the order and payment intent before the transaction. If the transaction arrives first, reconciliation becomes guesswork.

For merchants, the most important object is often not the transaction hash. It is the payment intent linked to the order. A transaction hash tells you what happened on-chain. A payment intent tells you what business event the transaction was supposed to satisfy.

Idempotency retries and confirmations

Agents retry. Networks delay. Webhooks duplicate. Users refresh. None of this is unusual.

Your API should support idempotency keys for agent-initiated payment requests. If an agent asks to create a payment intent twice for the same task, return the same active intent rather than creating two payable invoices.

Example request:

POST /payment-intents

Idempotency-Key: task_77_purchase_vendor_plan

Content-Type: application/json

Example behavior:

| Situation | Correct behavior |

|---|---|

| Same idempotency key, same payload | Return existing payment intent |

| Same key, different amount | Reject and require a new key or explicit update |

| Expired payment intent | Return expired state and allow fresh quote creation |

| Duplicate webhook | Acknowledge without re-fulfilling |

| Payment confirmed after expiry | Mark as late and route to review or refund logic |

Confirmation policy also matters. Low-value digital goods may fulfill after fewer confirmations or processor-level confidence. Higher-value orders may require deeper confirmation. The agent should not choose this policy. The merchant or payment platform should.

What works and what fails in production

What works

The patterns that work tend to be boring.

They use structured APIs instead of scraped checkout pages. They keep payment state in the backend. They enforce spending limits outside the prompt. They make webhooks idempotent. They preserve enough metadata for support and reconciliation. They design refunds before the first angry customer asks for one.

What works:

- Server-created payment intents with strict amount, asset, and expiry rules

- Agent metadata attached to every payment and order

- Policy enforcement before payment instructions are issued

- Webhook-driven fulfillment instead of frontend assumptions

- Balance or escrow models for repeated agent activity

- Human review queues for late, overpaid, underpaid, or suspicious payments

- Clear customer receipts that explain the agent action

A good agent payment implementation should feel uneventful. The agent asks. The backend validates. The payment layer tracks. The merchant system fulfills. Support can inspect the trail.

That is not flashy, but it is shippable.

What fails

What fails is usually a missing boundary.

The agent is allowed to construct arbitrary payment instructions. The wallet signs based on a natural language explanation. The merchant backend trusts a transaction hash without matching it to an order. Webhooks update state twice. Refunds are handled manually in a spreadsheet. Support cannot tell whether the user, agent, or merchant initiated the action.

Common failure modes:

| Failure mode | What breaks |

|---|---|

| Agent-created amounts | Overpayment, underpayment, wrong token, wrong chain |

| No expiry handling | Late payments get fulfilled incorrectly or lost in review |

| No idempotency | Duplicate invoices, duplicate fulfillment, duplicate support tickets |

| Prompt-only policy | Agent behavior drifts from backend authorization |

| No agent metadata | Support cannot explain the purchase |

| Transaction-first design | Reconciliation depends on manual matching |

| Weak webhook handling | Orders show paid before final confirmation or never update at all |

The hard part is not making an agent spend crypto once. The hard part is making a merchant comfortable with what happens on the thousandth payment, especially when the agent, user, network, and merchant system disagree.

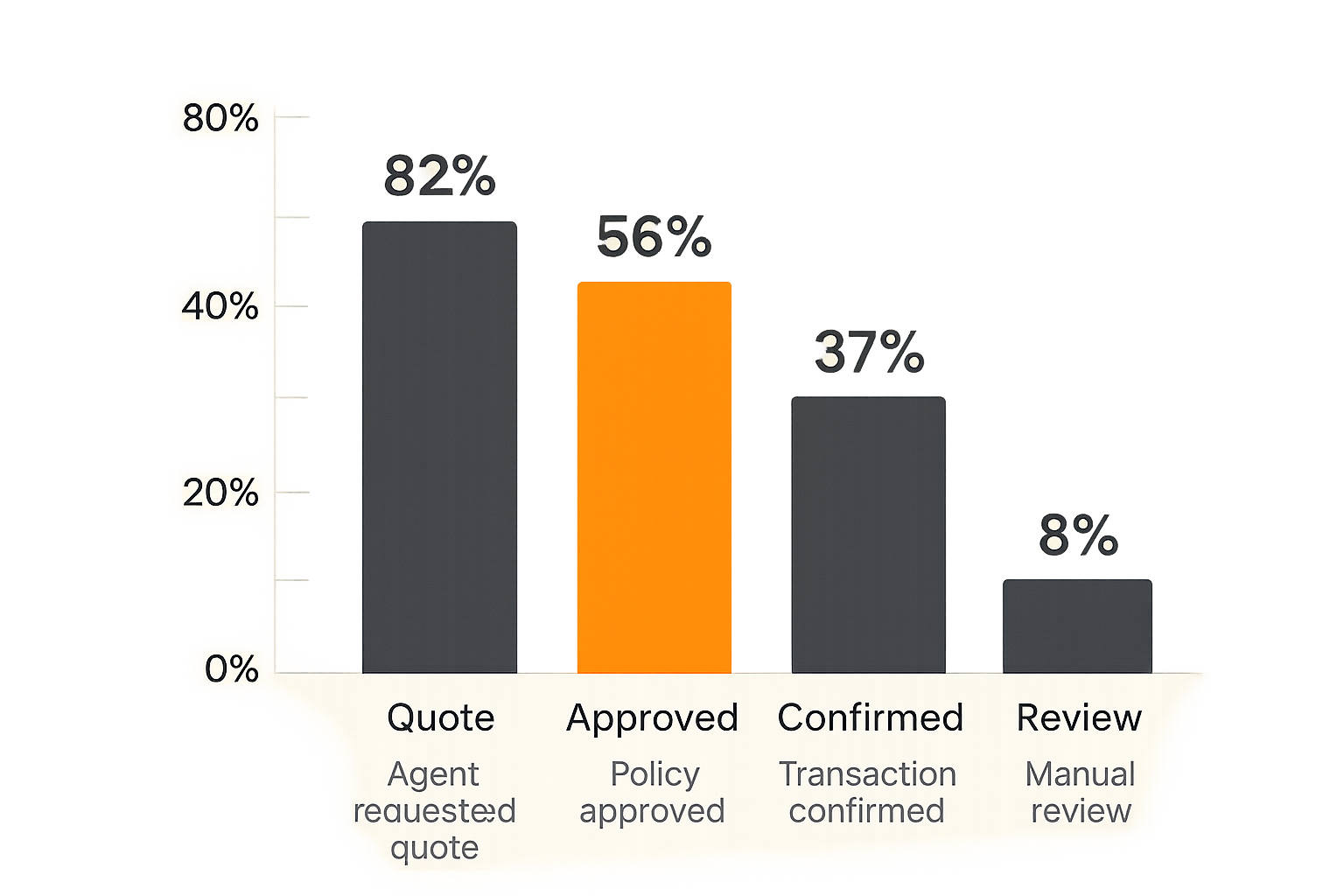

Metrics merchants should track for ai agents blockchain payments

Agent payment funnel

If agents become buyers, merchants need visibility into the agent payment funnel. Otherwise, you will not know whether failures come from agent reasoning, policy denial, wallet funding, network friction, or checkout design.

Track these events separately:

- Agent requested quote

- Payment intent created

- Policy approved

- Approval required

- Payment instruction delivered

- Transaction detected

- Transaction confirmed

- Order fulfilled

- Payment expired

- Payment failed

- Refund initiated

Do not collapse these into “checkout conversion.” Agent commerce has more states than a normal button flow. A policy denial is not the same as a wallet failure. A detected transaction is not the same as a confirmed payment. An expired quote is not the same as an abandoned cart.

A useful dashboard separates business outcomes from infrastructure outcomes:

| Metric | What it tells you |

|---|---|

| Quote-to-intent rate | Whether agents can understand and request purchasable offers |

| Intent-to-payment rate | Whether payment instructions are usable |

| Policy denial rate | Whether spend rules are too strict or agents are overreaching |

| Late payment rate | Whether expiry windows or agent workflows are misaligned |

| Manual review rate | Operational burden from edge cases |

| Refund rate | Quality of agent decisions and merchant expectations |

That changes the conversation with product teams. Instead of saying “agents do not convert,” you can say “agents request valid quotes, but 30% hit approval gates” or “most failures are late payments after quote expiry.” Use your own numbers, but instrument the states.

Exceptions that need human review

Agent payments need a review lane. Trying to automate every edge case on day one creates more risk than it removes.

Send these cases to human review or controlled automation:

- Payment received after expiry

- Underpayment or overpayment

- Wrong token or wrong network

- Multiple payments for one intent

- Payment from an unexpected wallet

- Merchant mismatch

- Policy changed during payment

- Refund requested for agent-initiated purchase

- High-value first-time merchant payment

The review tool should show the full context: user, agent, task, policy, order, payment intent, transaction hash, webhook history, and current fulfillment status. Without that context, human review becomes manual blockchain forensics.

Practical rule: if support cannot reconstruct the payment in two minutes, the system is missing operational context.

Security compliance and support realities

Abuse refunds and dispute handling

AI agents create new abuse paths because they can act quickly and repeatedly. A compromised agent session can attempt many small purchases. A malicious merchant can craft instructions that manipulate an agent into buying the wrong item. A buggy tool integration can loop payments until a balance is empty.

Security controls should include:

- Rate limits per agent, user, merchant, and policy

- Velocity checks on payment attempts

- Merchant allowlists for autonomous spending

- Risk scoring for new merchants

- Balance caps for hosted accounts

- Approval gates for unusual categories

- Webhook signature verification

- Separate permissions for creating intents and executing payments

Refunds also need design. In blockchain payments, a refund may be a new outbound transaction. That means you need to know where to refund, which asset to use, who approves it, and how it is recorded. If the original payer was an agent wallet, refunding to that wallet may not satisfy the human customer unless your ledger maps the wallet to the account.

Do not wait until support asks for a refund button. Build the refund state machine with the payment state machine.

Audit trails and merchant operations

Compliance requirements vary by jurisdiction and business model, so avoid pretending there is one universal answer. But operationally, every merchant needs a defensible audit trail.

At minimum, store:

- User or business account responsible for the payment

- Agent identity and version if available

- Tool call or task reference

- Payment policy applied at the time

- Merchant order and invoice reference

- Payment intent state history

- Blockchain transaction references

- Webhook event IDs and timestamps

- Approval records if human approval occurred

- Refund and adjustment records

The audit trail is not only for compliance. It is for debugging. When an agent purchases the wrong subscription tier, you need to know whether the prompt was ambiguous, the merchant API returned confusing data, the policy allowed too much, or the payment system fulfilled the wrong order.

This is where many demos collapse in production. They prove the happy path and ignore the operator path. Merchants do not just need payments to succeed. They need failed payments to be explainable.

How CoinPayPortal fits into the agent payment layer

Keep payment state outside the agent

For developers and merchants, the right payment gateway does not try to make the agent magical. It gives the agent a reliable payment interface while keeping payment state, confirmations, settlement, and merchant records outside the model.

That is the product-fit for CoinPayPortal in agent-driven commerce. The agent can request or interact with payment flows, but the merchant should still rely on a payment layer designed for crypto checkout, transaction tracking, webhooks, and settlement operations.

A clean integration looks like this:

- Agent identifies a purchase candidate.

- Merchant backend creates an order and payment intent.

- Payment layer returns structured payment instructions.

- Agent or wallet completes payment within policy.

- Webhooks update the merchant backend.

- Fulfillment happens from confirmed payment state.

- Reconciliation and support use the payment record, not the prompt transcript.

This architecture keeps the agent useful without making it dangerously authoritative. The agent can accelerate discovery and execution. The payment layer remains responsible for money movement state.

Build for merchants not demos

The demo version of ai agents blockchain payments is an agent that says, “I paid.”

The merchant version answers:

- Which order was paid?

- Was the amount exact?

- Which chain and token were used?

- Was the payment on time?

- Did the webhook arrive and process once?

- Has the order been fulfilled?

- Can support explain it?

- Can finance reconcile it?

- Can a refund be issued?

CoinPayPortal is most useful when treated as part of that merchant operating layer. Developers can build agent interfaces, SDKs, and automation around it, but the gateway should remain the source for payment instructions, payment lifecycle events, and merchant-facing status.

The goal is not to make every agent a bank. The goal is to let agents participate in commerce without weakening the payment controls merchants already need.

Closing checklist for ai agents blockchain payments

Architecture decisions to make now

If you are planning ai agents blockchain payments, make these decisions before writing the first wallet integration:

- Define your actor model: user, business, agent, session, policy.

- Choose the wallet boundary: user wallet, hosted balance, or policy wallet.

- Create payment intents server-side.

- Enforce spend policy outside the prompt.

- Use idempotency keys for agent-initiated requests.

- Treat webhooks as the source of truth.

- Store agent metadata on payment and order records.

- Build review queues for late, wrong, duplicate, and suspicious payments.

- Design refunds and reconciliation early.

- Give support a complete audit trail.

The mistake teams make is starting with the most exciting part: autonomous spending. Start with the least exciting part: state. If the state machine is sound, agents can become another channel. If the state machine is weak, agents amplify every failure.

The practical next step

The practical next step is to build one narrow agent payment flow with real operational boundaries.

Pick a low-risk use case: a small digital purchase, a prepaid API balance, or a test merchant invoice. Add policy limits. Add webhook processing. Add support visibility. Add refund handling. Then let the agent initiate the flow and see where the system strains.

You will learn more from one constrained production workflow than from ten open-ended demos.

AI agents blockchain payments will not be won by the flashiest wallet prompt. They will be won by teams that understand checkout architecture, settlement, custody boundaries, webhook reliability, and merchant operations.

Try coinpayportal.com

CoinPayPortal helps developers and merchants build crypto payment flows with practical checkout, transaction tracking, and merchant operations in mind. Try coinpayportal.com.

Try CoinPay

Non-custodial crypto payments — multi-chain, Lightning-ready, and fast to integrate.

Get started →